Data Preprocessing

Economic and financial time series data can require preprocessing or

transforming before you can analyze or model them. While base MATLAB® has general purpose and timetable functionality for

preprocessing or cleaning data (for example, the log function

removes an exponential trend from series and Data Cleaner

enables you to clean messy data interactively), Econometrics Toolbox™ has specialized functionality for preprocessing financial time

series. For example, you can obtain a common or desired time base by

aggregating multiple series, convert price series to growth rates, or

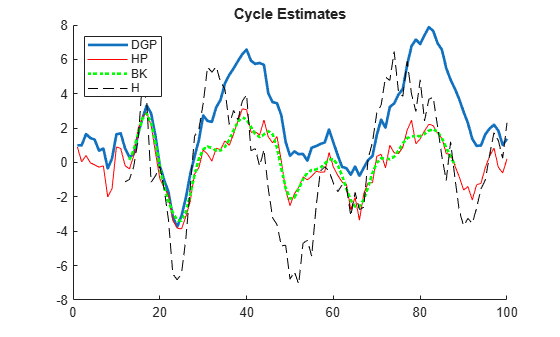

decompose series into additive trend and cyclical components.

Apps

| Econometric Modeler | Analyze and model econometric time series |

Classes

LagOp | Create lag operator polynomial |

Functions

Topics

Interactive Workflows

- Prepare Time Series Data for Econometric Modeler App

Prepare time series data at the MATLAB command line, and then import the set into Econometric Modeler. - Import Time Series Data into Econometric Modeler App

Import time series data from the MATLAB Workspace or a MAT-file into Econometric Modeler. - Plot Time Series Data Using Econometric Modeler App

Interactively plot univariate and multivariate time series data, then interpret and interact with the plots. - Transform Time Series Using Econometric Modeler App

Transform time series data interactively. - Analyze Time Series Data Using Econometric Modeler

Interactively visualize and analyze univariate or multivariate time series data.

Transform Time Series Data

- Nonseasonal Differencing

Take a nonseasonal difference of a time series. - Nonseasonal and Seasonal Differencing

Apply both nonseasonal and seasonal differencing using lag operator polynomial objects. - Econometric Modeling

Understand model-selection techniques and Econometrics Toolbox features. - Stochastic Process Characteristics

Understand the definition, forms, and properties of stochastic processes. - Data Transformations

Determine which data transformations are appropriate for your problem. - Trend-Stationary vs. Difference-Stationary Processes

Determine the characteristics of nonstationary processes. - Time Base Partitions for ARIMA Model Estimation

When you fit a time series model to data, lagged terms in the model require initialization, usually with observations at the beginning of the sample.

Decompose Time Series Data

- Decompose Time Series Into Additive Trend Components

Estimate nonseasonal and seasonal trend components using parametric models. - Estimate Moving Average Trend Using Moving Average Filter

This example shows how to estimate long-term trend using a symmetric moving average function. - Seasonal Filters

You can use a seasonal filter (moving average) to estimate the seasonal component of a time series. - Seasonal Adjustment

Seasonal adjustment is the process of removing a nuisance periodic component. The result of a seasonal adjustment is a deseasonalized time series. - Seasonal Adjustment Using a Stable Seasonal Filter

Deseasonalize a time series using a stable seasonal filter. - Seasonal Adjustment Using S(n,m) Seasonal Filters

Apply seasonal filters to deseasonalize a time series. - Use Hodrick-Prescott Filter to Reproduce Original Result

Use the Hodrick-Prescott filter to decompose a time series. - Compare One-Sided and Two-Sided Hodrick-Prescott Filter Results

Smooth the U.S. GDP by applying the one-sided and two-sided Hodrick-Prescott filters, and compare the resulting smoothed trends.

Lag Operator Polynomial Operations

- Specify Lag Operator Polynomials

Create lag operator polynomial objects.

Related Information

Featured Examples

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)