filter

Filter disturbances through regression model with ARIMA errors

Description

Y = filter(Mdl,Z)Y resulting

from filtering the numeric array of one or more underlying disturbance series

Z through the fully specified, univariate regression model with

ARIMA errors Mdl. Z is associated with the error

model innovations process that drives the specified regression model with ARIMA

errors.

Tbl2 = filter(Mdl,Tbl1)Tbl2 containing the results from

filtering the paths of disturbances in the input table or timetable

Tbl1 through Mdl. The disturbance variable in

Tbl1 is associated with the model innovations process that drives

Mdl. (since R2023b)

filter selects the variable

Mdl.SeriesName, or the sole variable in Tbl1, as

the disturbance variable to filter through the model. To select a different variable in

Tbl1 to filter through the model, use the

DisturbanceVariable name-value argument.

[___] = filter(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name,Value)filter returns the output argument combination for the

corresponding input arguments. For example, filter(Mdl,Z,X=Pred,Z0=PSZ) specifies the

predictor data Pred for the model regression component and the

observed errors in the presample period PSZ to initialize the

model.

Examples

Filter Disturbance Vector to Compute Impulse Response Function

Compute the impulse response function (IRF) of an innovation shock to the regression model with ARMA(2,1) errors. Supply the innovation shock as a vector.

The IRF assesses the dynamic behavior of a system to a one-time shock. Typically, the magnitude of the shock is 1. Alternatively, it might be more meaningful to examine an IRF of an innovation shock with a magnitude of one standard deviation.

In regression models with ARIMA errors,

The IRF is invariant to the behavior of the predictors and the intercept.

The IRF of the model is defined as the impulse response of the unconditional disturbances as governed by the ARIMA error component.

Create the following regression model with ARMA(2,1) errors:

where is Gaussian with variance 0.1.

Mdl = regARIMA(Intercept=0,AR={0.5 -0.8},MA=-0.5, ...

Variance=0.1);When you construct an impulse response function for a regression model with ARIMA errors, you must set Intercept to 0.

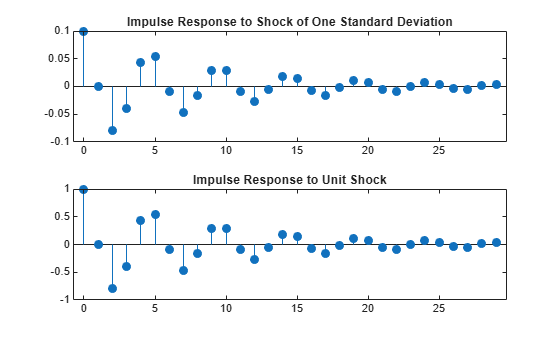

Simulate the first 30 responses of the impulse response function by generating a error series with a one-time impulse with magnitude equal to one standard deviation, and then filter it. Also, use impulse to compute the IRF.

z = [sqrt(Mdl.Variance); zeros(29,1)]; % Shock of 1 std

yFltr = filter(Mdl,z);

yImpls = impulse(Mdl,30);When you construct an IRF of a regression model with ARIMA errors containing a regression component, do not specify the predictor matrix, X, in filter.

Plot the IRFs.

figure tiledlayout(2,1) nexttile stem((0:numel(yFltr)-1)',yFltr,"filled") title("Impulse Response to Shock of One Standard Deviation") nexttile stem((0:numel(yImpls)-1)',yImpls,"filled") title("Impulse Response to Unit Shock")

The IRF given a shock of one standard deviation is a scaled version of the IRF returned by impulse.

Compute Step Response

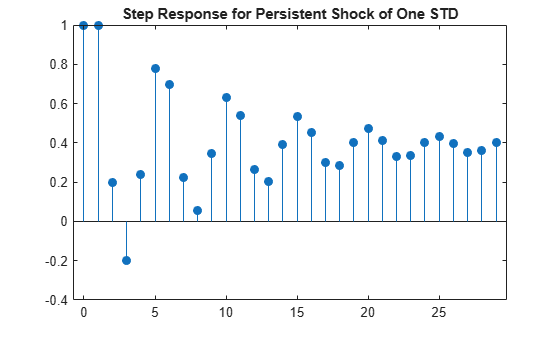

Compute the step response function of a regression model with ARMA(2,1) errors.

The step response assesses the dynamic behavior of a system to a persistent shock. Typically, the magnitude of the shock is 1. Alternatively, it might be more meaningful to examine a step response of a persistent innovation shock with a magnitude of one standard deviation. This example plots the step response of a persistent innovations shock in a model without an intercept and predictor matrix for regression. However, note that filter is flexible in that it accepts a persistent innovations or predictor shock that you construct using any magnitude, then filters it through the model.

Specify the following regression model with ARMA(2,1) errors:

where is Gaussian with variance 0.1.

Mdl = regARIMA(Intercept=0,AR={0.5 -0.8},MA=-0.5, ...

Variance=0.1);Compute the first 30 responses to a sequence of unit errors by generating an error series of one standard deviation, and then filtering it.

z = sqrt(Mdl.Variance)*ones(30,1); % Persistent shock of one std y = filter(Mdl,z); y = y/y(1); % Normalize relative to y(1)

Plot the step response function.

figure stem((0:numel(y)-1)',y,"filled") title("Step Response for Persistent Shock of One STD")

The step response settles around 0.4.

Filter Timetable of Disturbances Through Estimated Model

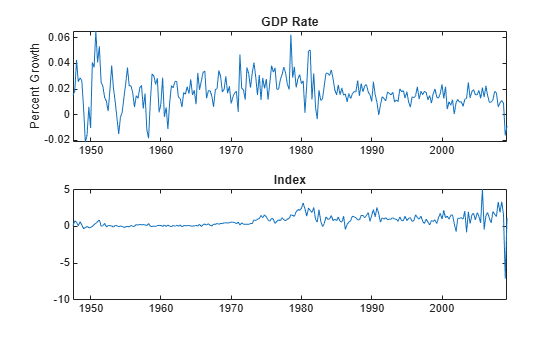

Fit a regression model with ARMA(1,1) errors by regressing the US consumer price index (CPI) quarterly changes onto the US gross domestic product (GDP) growth rate. Supply a timetable of data and specify the series for the fit. Then, filter paths of disturbances in a timetable through the fitted model.

Load and Transform Data

Load the US macroeconomic data set. Compute the series of GDP quarterly growth rates and CPI quarterly changes.

load Data_USEconModel DTT = price2ret(DataTimeTable,DataVariables="GDP"); DTT.GDPRate = 100*DTT.GDP; DTT.CPIDel = diff(DataTimeTable.CPIAUCSL); T = height(DTT)

T = 248

figure tiledlayout(2,1) nexttile plot(DTT.Time,DTT.GDPRate) title("GDP Rate") ylabel("Percent Growth") nexttile plot(DTT.Time,DTT.CPIDel) title("Index")

The series appear stationary, albeit heteroscedastic.

Prepare Timetable for Estimation

When you plan to supply a timetable, you must ensure it has all the following characteristics:

The selected response variable is numeric and does not contain any missing values.

The timestamps in the

Timevariable are regular, and they are ascending or descending.

Remove all missing values from the timetable.

DTT = rmmissing(DTT); T_DTT = height(DTT)

T_DTT = 248

Because each sample time has an observation for all variables, rmmissing does not remove any observations.

Determine whether the sampling timestamps have a regular frequency and are sorted.

areTimestampsRegular = isregular(DTT,"quarters")areTimestampsRegular = logical

0

areTimestampsSorted = issorted(DTT.Time)

areTimestampsSorted = logical

1

areTimestampsRegular = 0 indicates that the timestamps of DTT are irregular. areTimestampsSorted = 1 indicates that the timestamps are sorted. Macroeconomic series in this example are timestamped at the end of the month. This quality induces an irregularly measured series.

Remedy the time irregularity by shifting all dates to the first day of the quarter.

dt = DTT.Time; dt = dateshift(dt,"start","quarter"); DTT.Time = dt; areTimestampsRegular = isregular(DTT,"quarters")

areTimestampsRegular = logical

1

DTT is regular.

Create Model Template for Estimation

Suppose that a regression model of CPI quarterly changes onto the GDP rate, with ARMA(1,1) errors, is appropriate.

Create a model template for a regression model with ARMA(1,1) errors template.

Mdl = regARIMA(1,0,1)

Mdl =

regARIMA with properties:

Description: "ARMA(1,1) Error Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

Intercept: NaN

Beta: [1×0]

P: 1

Q: 1

AR: {NaN} at lag [1]

SAR: {}

MA: {NaN} at lag [1]

SMA: {}

Variance: NaN

Mdl is a partially specified regARIMA object.

Fit Model to Data

Fit a regression model with ARMA(1,1) errors to the data. Specify the entire series GDP rate and CPI quarterly changes series, and specify the response and predictor variable names.

EstMdl = estimate(Mdl,DTT,ResponseVariable="GDPRate", ... PredictorVariables="CPIDel");

Regression with ARMA(1,1) Error Model (Gaussian Distribution):

Value StandardError TStatistic PValue

________ _____________ __________ __________

Intercept 0.0162 0.0016077 10.077 6.9995e-24

AR{1} 0.60515 0.089912 6.7305 1.6906e-11

MA{1} -0.16221 0.11051 -1.4678 0.14216

Beta(1) 0.002221 0.00077691 2.8587 0.0042532

Variance 0.000113 7.2753e-06 15.533 2.0838e-54

EstMdl is a fully specified, estimated regARIMA object.

Filter Random Gaussian Disturbance Paths

Generate 2 random, independent series of length T_DTT from the standard Gaussian distribution. Store the matrix of series as one variable in DTT.

rng(1,"twister") % For reproducibility DTT.Z = randn(T_DTT,2);

DTT contains a new variable called Z containing a T_DTT-by-2 matrix of two disturbance paths.

Filter the paths of disturbances through the estimated model. Specify the table variable name containing the disturbance paths.

Tbl2 = filter(EstMdl,DTT,DisturbanceVariable="Z");

tail(Tbl2) Time Interval GDP GDPRate CPIDel Z Y_Response Y_ErrorInnovation Y_RegressionInnovation

_____ ________ ___________ __________ ______ ______________________ ______________________ __________________________ __________________________

Q2-07 91 0.00018278 0.018278 1.675 -0.36436 -0.7055 0.016068 0.0071243 -0.0038733 -0.0074997 -0.0001316 -0.0090757

Q3-07 91 0.00016916 0.016916 1.359 -0.093312 -0.3311 0.015757 0.0084046 -0.00099194 -0.0035197 -0.00044331 -0.0077954

Q4-07 94 6.1286e-05 0.0061286 3.355 0.48981 -1.5208 0.021299 -0.0041131 0.0052068 -0.016167 0.0050995 -0.020313

Q1-08 91 9.3272e-05 0.0093272 1.93 1.4014 0.16528 0.033339 0.0082868 0.014898 0.001757 0.017139 -0.0079132

Q2-08 91 0.00011103 0.011103 3.367 -0.27422 -0.48787 0.02124 0.00594 -0.0029151 -0.0051862 0.0050402 -0.01026

Q3-08 92 8.9585e-05 0.0089585 1.641 0.67582 0.58697 0.026907 0.017072 0.0071842 0.0062397 0.010707 0.00087209

Q4-08 92 -0.00016145 -0.016145 -7.098 0.19058 -0.90337 0.02354 0.0061124 0.0020259 -0.0096032 0.00734 -0.010088

Q1-09 90 -8.6878e-05 -0.0086878 1.137 0.67036 0.37101 0.027439 0.015597 0.0071262 0.003944 0.011239 -0.00060284

size(Tbl2)

ans = 1×2

248 8

Tbl2 is a 248-by-8 timetable containing all variables in DTT, and the two filtered response paths Y_Response, error model innovation paths Y_ErrorInnovation, and unconditional disturbance paths Y_RegressionInnovation.

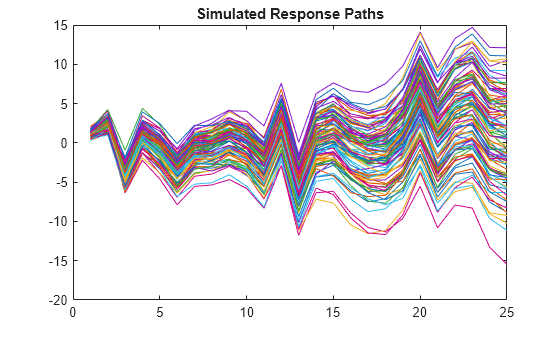

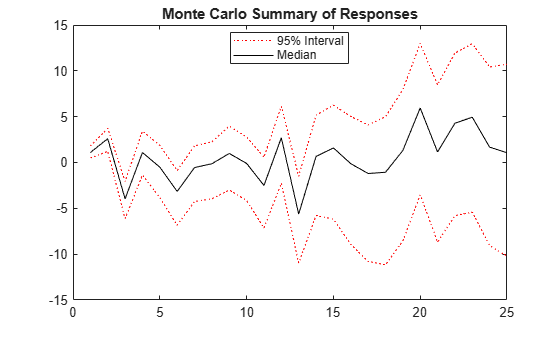

Filter Error Paths Through Regression Model with SARIMA Errors

Simulate 100 independent paths of responses by filtering 100 independent paths of errors , where innovations , through the following regression model with SARIMA errors.

where follows a -distribution with 15 degrees of freedom.

Distribution = struct("Name","t","DoF",15); Mdl = regARIMA(AR={0.2 0.1},SAR=0.01,SARLags=12, ... MA=0.5,SMA=0.02,SMALags=12,D=1,Seasonality=12, ... Beta=[1.5; -2],Intercept=0,Variance=0.1, ... Distribution=Distribution)

Mdl =

regARIMA with properties:

Description: "Regression with ARIMA(2,1,1) Error Model Seasonally Integrated with Seasonal AR(12) and MA(12) (t Distribution)"

SeriesName: "Y"

Distribution: Name = "t", DoF = 15

Intercept: 0

Beta: [1.5 -2]

P: 27

D: 1

Q: 13

AR: {0.2 0.1} at lags [1 2]

SAR: {0.01} at lag [12]

MA: {0.5} at lag [1]

SMA: {0.02} at lag [12]

Seasonality: 12

Variance: 0.1

Simulate a length 25 path of data from the standard bivariate normal distribution for the predictor variables in the regression component.

rng(1,"twister") % For reproducibility numObs = 25; Pred = randn(numObs,2);

Simulate 100 independent paths of errors of length 25 from the standard normal distribution.

numPaths = 100; Z = randn(numObs,numPaths);

Simulate 100 independent response paths from model by filtering the paths of errors through the model. Supply the predictor data for the regression component.

Y = filter(Mdl,Z,X=Pred);

figure

plot(Y)

title("Simulated Response Paths")

Plot the 2.5th, 50th (median), and 97.5th percentiles of the simulated response paths.

lower = prctile(Y,2.5,2); middle = median(Y,2); upper = prctile(Y,97.5,2); figure plot(1:25,lower,"r:",1:25,middle,"k", ... 1:25,upper,"r:") title("Monte Carlo Summary of Responses") legend("95% Interval","Median",Location="best")

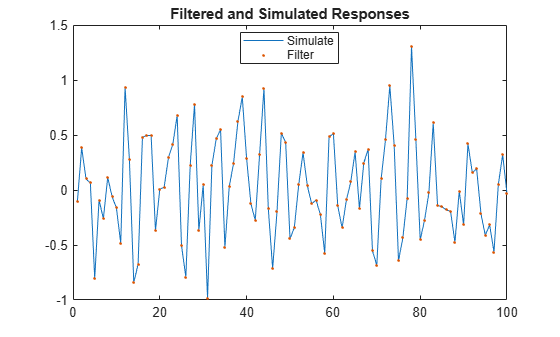

Compare Responses from filter and simulate

Simulate responses using filter and simulate. Then compare the simulated responses.

Both filter and simulate filter a series of errors to produce output responses y, innovations e, and unconditional disturbances u. The difference is that simulate generates errors from Mdl.Distribution, whereas filter accepts a random array of errors that you generate from any distribution.

Specify the following regression model with ARMA(2,1) errors:

where is Gaussian with variance 0.1.

Mdl = regARIMA(Intercept=0,AR={0.5 -0.8},MA=-0.5, ...

Beta=[0.1 -0.2],Variance=0.1);Mdl is a fully specified regARIMA object.

Simulate a one path of bivariate standard normal data for the predictor variables. Then, simulate a path of responses and innovations from the regression model with ARMA(2,1) errors. Supply the simulated predictor data to simulate for the regression component.

rng(1,"twister") % For reproducibility Pred = randn(100,2); % Simulate predictor data [ySim,eSim] = simulate(Mdl,100,X=Pred);

ySim and eSIM are 100-by-1 vectors of simulated responses and innovations, respectively, from the model Mdl.

Produce model errors by standardizing the simulated innovations. Filter the simulated errors through the model. Supply the predictor data to filter.

z1 = eSim./sqrt(Mdl.Variance); yFlt1 = filter(Mdl,z1,X=Pred);

yFlt1 is a 100-by-1 vector of responses resulting from filtering the simulated errors z1 through the model Mdl.

Confirm that the simulated responses from simulate and filter are identical by plotting the two series.

figure h1 = plot(ySim); hold on h2 = plot(yFlt1,"."); title("Filtered and Simulated Responses") legend([h1 h2],["Simulate" "Filter"],Location="best") hold off

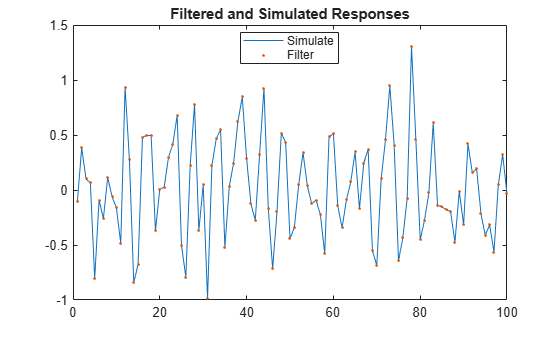

Alternatively, simulate responses by randomly generating your own errors and passing them into filter.

rng(1,"twister") Pred = randn(100,2); z2 = randn(100,1); yFlt2 = filter(Mdl,z2,X=Pred); figure h1 = plot(ySim); hold on h2 = plot(yFlt2,"."); title("Filtered and Simulated Responses") legend([h1 h2],["Simulate" "Filter"],Location="best") hold off

This plot is the same as the previous plot, confirming that both simulation methods are equivalent.

filter multiplies the error, Z, by sqrt(Mdl.Variance) before filtering Z through the model. Therefore, if you want to specify a different distribution, set Mdl.Variance to 1, and then generate your own errors using, for example, random("unif",a,b) for the Uniform(a, b) distribution.

Input Arguments

Output Arguments

Alternative Functionality

filter generalizes simulate. Both filter a series of errors to produce responses

Y, innovations E, and unconditional disturbances

U. However, simulate autogenerates

a series of mean zero, unit variance, independent and identically distributed (iid) errors

according to the distribution in Mdl. In contrast,

filter requires that you specify your own errors, which can come

from any distribution.

References

[1] Box, G. E. P., G. M. Jenkins, and G. C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[2] Davidson, R., and J. G. MacKinnon. Econometric Theory and Methods. Oxford, UK: Oxford University Press, 2004.

[3] Enders, Walter. Applied Econometric Time Series. Hoboken, NJ: John Wiley & Sons, Inc., 1995.

[4] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[5] Pankratz, A. Forecasting with Dynamic Regression Models. John Wiley & Sons, Inc., 1991.

[6] Tsay, R. S. Analysis of Financial Time Series. 2nd ed. Hoboken, NJ: John Wiley & Sons, Inc., 2005.

Version History

Introduced in R2013bSee Also

Objects

Functions

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)