simulate

Monte Carlo simulation of vector autoregression (VAR) model

Syntax

Description

Conditional and Unconditional Simulation for Numeric Arrays

Y = simulate(Mdl,numobs,Name=Value)simulate returns numeric arrays when all optional

input data are numeric arrays. For example,

simulate(Mdl,100,NumPaths=1000,Y0=PS) returns a numeric

array of 1000, 100-period simulated response paths from

Mdl and specifies the numeric array of presample

response data PS.

To produce a conditional simulation, specify response data in the simulation

horizon by using the YF name-value argument.

Unconditional Simulation for Tables and Timetables

Tbl = simulate(Mdl,numobs,Presample=Presample)Tbl containing the random

multivariate response and innovations variables, which results from the

unconditional simulation of the response series in the model

Mdl. simulate uses the table or

timetable of presample data Presample to initialize the

response series. (since R2022b)

simulate selects the variables in

Mdl.SeriesNames to simulate, or it selects all variables

in Presample. To select different response variables in

Tbl to simulate, use the

PresampleResponseVariables name-value argument.

Tbl = simulate(Mdl,numobs,Presample=Presample,Name=Value)simulate(Mdl,100,Presample=PSTbl,PresampleResponseVariables=["GDP"

"CPI"]) returns a timetable of variables containing 100-period

simulated response and innovations series from Mdl,

initialized by the data in the GDP and CPI

variables of the timetable of presample data in PSTbl. (since R2022b)

Conditional Simulation for Tables and Timetables

Tbl = simulate(Mdl,numobs,InSample=InSample,ResponseVariables=ResponseVariables)Tbl containing the random

multivariate response and innovations variables, which results from the

conditional simulation of the response series in the model

Mdl. InSample is a table or

timetable of response or predictor data in the simulation horizon that

simulate uses to perform the conditional simulation

and ResponseVariables specifies the response variables in

InSample. (since R2022b)

Tbl = simulate(___,Name=Value)

Examples

Return Response Series in Matrix from Unconditional Simulation

Fit a VAR(4) model to the consumer price index (CPI) and unemployment rate data. Then, simulate a vector of responses from the estimated model.

Load the Data_USEconModel data set.

load Data_USEconModelPlot the two series on separate plots.

figure plot(DataTimeTable.Time,DataTimeTable.CPIAUCSL); title("Consumer Price Index") ylabel("Index") xlabel("Date")

figure plot(DataTimeTable.Time,DataTimeTable.UNRATE); title("Unemployment Rate") ylabel("Percent") xlabel("Date")

Stabilize the CPI by converting it to a series of growth rates. Synchronize the two series by removing the first observation from the unemployment rate series. Create a new data set containing the transformed variables, and do not include any rows containing at least one missing observation.

rcpi = price2ret(DataTimeTable.CPIAUCSL); unrate = DataTimeTable.UNRATE(2:end); dates = DataTimeTable.Time(2:end); Data = array2timetable([rcpi unrate],RowTimes=dates, ... VariableNames=["RCPI" "UNRATE"]); Data = rmmissing(Data);

Create a default VAR(4) model by using the shorthand syntax.

Mdl = varm(2,4); Mdl.SeriesNames = Data.Properties.VariableNames;

Estimate the model using the entire data set.

EstMdl = estimate(Mdl,Data.Variables);

EstMdl is a fully specified, estimated varm model object.

Simulate a response series path from the estimated model with length equal to the path in the data.

rng(1); % For reproducibility

numobs = height(Data);

Y = simulate(EstMdl,numobs);Y is a 245-by-2 matrix of simulated responses. The first and second columns contain the simulated CPI growth rate and unemployment rate, respectively.

Plot the simulated and true responses.

figure plot(Data.Time,Y(:,1)); hold on plot(Data.Time,Data.RCPI) title("CPI Growth Rate"); ylabel("Growth Rate") xlabel("Date") legend("Simulation","Observed") hold off

figure plot(Data.Time,Y(:,2)); hold on plot(Data.Time,Data.UNRATE) ylabel("Percent") xlabel("Date") title("Unemployment Rate") legend("Simulation","Observed") hold off

Simulate Responses Using filter

Illustrate the relationship between simulate and filter by estimating a 4-D VAR(2) model of the four response series in Johansen's Danish data set. Simulate a single path of responses using the fitted model and the historical data as initial values, and then filter a random set of Gaussian disturbances through the estimated model using the same presample responses.

Load Johansen's Danish economic data.

load Data_JDanishFor details on the variables, enter Description.

Create a default 4-D VAR(2) model.

Mdl = varm(4,2); Mdl.SeriesNames = DataTimeTable.Properties.VariableNames;

Estimate the VAR(2) model using the entire data set.

EstMdl = estimate(Mdl,DataTimeTable.Variables);

When reproducing the results of simulate and filter:

Set the same random number seed using

rng.Specify the same presample response data using the

Y0name-value argument.

Set the default random seed. Simulate 100 observations by passing the estimated model to simulate. Specify the entire data set as the presample.

rng("default")

YSim = simulate(EstMdl,100,Y0=DataTimeTable.Variables);YSim is a 100-by-4 matrix of simulated responses. Columns correspond to the columns of the variables in Data.

Set the default random seed. Simulate 4 series of 100 observations from the standard Gaussian distribution.

rng("default")

Z = randn(100,4);Filter the Gaussian values through the estimated model. Specify the entire data set as the presample.

YFilter = filter(EstMdl,Z,Y0=DataTimeTable.Variables);

YFilter is a 100-by-4 matrix of simulated responses. Columns correspond to the columns of the variables in the data Data. Before filtering the disturbances, filter scales Z by the lower triangular Cholesky factor of the model covariance in EstMdl.Covariance.

Compare the resulting responses between filter and simulate.

(YSim - YFilter)'*(YSim - YFilter)

ans = 4×4

0 0 0 0

0 0 0 0

0 0 0 0

0 0 0 0

The results are identical.

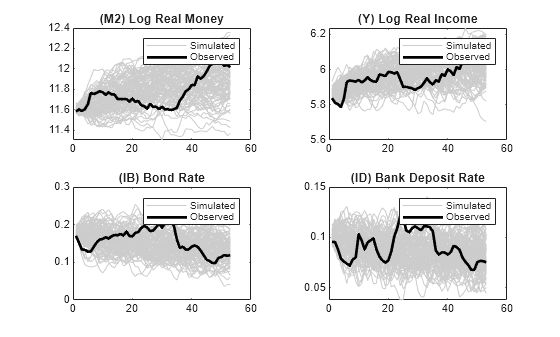

Simulate Arrays of Multiple Response and Innovations Paths

Load Johansen's Danish economic data. Remove all missing observations.

load Data_JDanish

Data = rmmissing(Data);

T = height(Data);For details on the variables, enter Description.

Create a default 4-D VAR(2) model.

Mdl = varm(4,2);

Estimate the VAR(2) model using the entire data set.

EstMdl = estimate(Mdl,Data);

When reproducing the results of simulate and filter:

Set the same random number seed using

rng.Specify the same presample response data using the

Y0name-value argument.

Simulate 100 paths of T – EstMdl.P, the effective sample size, responses, and corresponding innovations by passing the estimated model to simulate. Specify the same matrix of presample as the presample used in estimation (the earliest Mdl.P observations, by default).

rng("default")

p = Mdl.P;

numobs = T - p;

PS = Data(1:p,:);

[YSim,ESim] = simulate(EstMdl,numobs,NumPaths=100,Y0=PS);

size(YSim)ans = 1×3

53 4 100

YSim and ESim are 53-by-4-by-1000 numeric arrays of simulated responses and innovations, respectively. Each row corresponds to a period in the simulation horizon, each column corresponds to the variable in EstMdl.SeriesNames, and pages are separate, independently simulated paths.

Plot each simulated response and innovations variable with their observations.

figure InSample = Data((p+1):end,:); tiledlayout(2,2) for j = 1:numel(EstMdl.SeriesNames) nexttile h1 = plot(squeeze(YSim(:,j,:)),Color=[0.8 0.8 0.8]); hold on h2 = plot(InSample(:,j),Color="k",LineWidth=2); hold off title(series(j)) legend([h1(1) h2],["Simulated" "Observed"]) end

E = infer(EstMdl,InSample,Y0=PS); figure tiledlayout(2,2) for j = 1:numel(EstMdl.SeriesNames) nexttile h1 = plot(squeeze(ESim(:,j,:)),Color=[0.8 0.8 0.8]); hold on h2 = plot(E(:,j),Color="k",LineWidth=2); hold off title("Innovations: " + EstMdl.SeriesNames{j}) legend([h1(1) h2],["Simulated" "Observed"]) end

Return Timetable of Responses and Innovations from Unconditional Simulation

Since R2022b

Fit a VAR(4) model to the consumer price index (CPI) and unemployment rate data. Then, perform an unconditional simulation of the estimated model and return the simulated responses and corresponding innovations in a timetable. This example is based on Return Response Series in Matrix from Unconditional Simulation.

Load and Preprocess Data

Load the Data_USEconModel data set. Compute the CPI growth rate. Because the growth rate calculation consumes the earliest observation, include the rate variable in the timetable by prepending the series with NaN.

load Data_USEconModel

DataTimeTable.RCPI = [NaN; price2ret(DataTimeTable.CPIAUCSL)];

T = height(DataTimeTable)T = 249

Prepare Timetable for Estimation

When you plan to supply a timetable directly to estimate, you must ensure it has all the following characteristics:

All selected response variables are numeric and do not contain any missing values.

The timestamps in the

Timevariable are regular, and they are ascending or descending.

Remove all missing values from the table, relative to the CPI rate (RCPI) and unemployment rate (UNRATE) series.

varnames = ["RCPI" "UNRATE"]; DTT = rmmissing(DataTimeTable,DataVariables=varnames); T = height(DTT)

T = 245

rmmissing removes the four initial missing observations from the DataTimeTable to create a sub-table DTT. The variables RCPI and UNRATE of DTT do not have any missing observations.

Determine whether the sampling timestamps have a regular frequency and are sorted.

areTimestampsRegular = isregular(DTT,"quarters")areTimestampsRegular = logical

0

areTimestampsSorted = issorted(DTT.Time)

areTimestampsSorted = logical

1

areTimestampsRegular = 0 indicates that the timestamps of DTT are irregular. areTimestampsSorted = 1 indicates that the timestamps are sorted. Macroeconomic series in this example are timestamped at the end of the month. This quality induces an irregularly measured series.

Remedy the time irregularity by shifting all dates to the first day of the quarter.

dt = DTT.Time; dt = dateshift(dt,"start","quarter"); DTT.Time = dt; areTimestampsRegular = isregular(DTT,"quarters")

areTimestampsRegular = logical

1

DTT is regular with respect to time.

Create Model Template for Estimation

Create a default VAR(4) model by using the shorthand syntax. Specify the response variable names.

Mdl = varm(2,4); Mdl.SeriesNames = varnames;

Fit Model to Data

Estimate the model. Pass the entire timetable DTT. By default, estimate selects the response variables in Mdl.SeriesNames to fit to the model. Alternatively, you can use the ResponseVariables name-value argument.

EstMdl = estimate(Mdl,DTT); p = EstMdl.P

p = 4

Perform Unconditional Simulation of Estimated Model

Simulate a response and innovations path from the estimated model and return the simulated series as variables in a timetable. simulate requires information for the output timetable, such as variable names, sampling times for the simulation horizon, and sampling frequency. Therefore, supply a presample of the earliest p = 4 observations of the data DTT, from which simulate infers the required timetable information. Specify a simulation horizon of numobs – p.

rng(1) % For reproducibility

PSTbl = DTT(1:p,:);

numobs = T - p;

Tbl = simulate(EstMdl,T,Presample=PSTbl);

size(Tbl)ans = 1×2

245 4

PSTbl

PSTbl=4×15 timetable

Time COE CPIAUCSL FEDFUNDS GCE GDP GDPDEF GPDI GS10 HOANBS M1SL M2SL PCEC TB3MS UNRATE RCPI

_____ _____ ________ ________ ____ _____ ______ ____ ____ ______ ____ ____ _____ _____ ______ _________

Q1-48 137.9 23.5 NaN 37.6 260.4 16.111 45 NaN 55.036 NaN NaN 170.5 1 4 0.0038371

Q2-48 139.6 24.15 NaN 39.7 267.3 16.254 48.1 NaN 55.007 NaN NaN 174.3 1 3.6 0.027284

Q3-48 144.5 24.36 NaN 41.4 273.9 16.556 50.2 NaN 55.398 NaN NaN 177.2 1.09 3.8 0.0086581

Q4-48 145.9 24.05 NaN 43.5 275.2 16.597 49.1 NaN 54.885 NaN NaN 178.1 1.16 4 -0.012807

head(Tbl)

Time RCPI_Responses UNRATE_Responses RCPI_Innovations UNRATE_Innovations

_____ ______________ ________________ ________________ __________________

Q1-49 0.0037294 4.6036 -0.0038547 0.25039

Q2-49 0.0064827 5.0083 0.0070154 0.027504

Q3-49 -0.0073358 5.4981 -0.0045047 0.25199

Q4-49 -0.0057328 5.7007 -0.0065904 0.10593

Q1-50 -0.0060454 5.8687 -0.005022 0.13824

Q2-50 -0.0084475 5.5758 -0.0034013 -0.26192

Q3-50 -0.0067066 5.4129 -0.0033182 0.13055

Q4-50 -0.0020759 5.2191 0.0010595 0.11135

Tbl is a 241-by-4 matrix of simulated responses and innovations. RCPI_Responses is the simulated path of the CPI growth rate and RCPI_Innovations is the corresponding innovations series, and the variables associated with the unemployment rate are similar. The timestamps of Tbl follow directly from the timestamps of PSTbl, and they have the same sampling frequency.

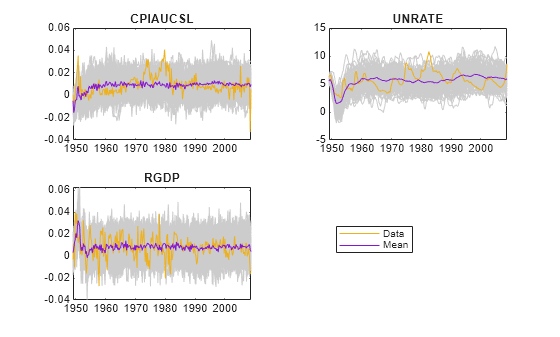

Simulate Responses from Model Containing Regression Component

Since R2022b

Estimate a VAR(4) model of the consumer price index (CPI), the unemployment rate, and the gross domestic product (GDP). Include a linear regression component containing the current and the last four quarters of government consumption expenditures and investment. Simulate multiple paths from the estimated model.

Load the Data_USEconModel data set. Compute the real GDP.

load Data_USEconModel

DataTimeTable.RGDP = DataTimeTable.GDP./DataTimeTable.GDPDEF*100;Plot all variables on separate plots.

figure tiledlayout(2,2) nexttile plot(DataTimeTable.Time,DataTimeTable.CPIAUCSL); ylabel("Index") title("Consumer Price Index") nexttile plot(DataTimeTable.Time,DataTimeTable.UNRATE); ylabel("Percent") title("Unemployment Rate") nexttile plot(DataTimeTable.Time,DataTimeTable.RGDP); ylabel("Output") title("Real Gross Domestic Product") nexttile plot(DataTimeTable.Time,DataTimeTable.GCE); ylabel("Billions of $") title("Government Expenditures")

Stabilize the CPI, GDP, and GCE by converting each to a series of growth rates. Synchronize the unemployment rate series with the others by removing its first observation.

varnames = ["CPIAUCSL" "RGDP" "GCE"]; DTT = varfun(@price2ret,DataTimeTable,InputVariables=varnames); DTT.Properties.VariableNames = varnames; DTT.UNRATE = DataTimeTable.UNRATE(2:end);

Make the time base regular.

dt = DTT.Time; dt = dateshift(dt,"start","quarter"); DTT.Time = dt;

Expand the GCE rate series to a matrix that includes the first lagged series through the fourth lag series.

RGCELags = lagmatrix(DTT,1:4,DataVariables="GCE");

DTT = [DTT RGCELags];

DTT = rmmissing(DTT);Create separate presample and estimation sample data sets. The presample contains the earliest p = 4 observations, and the estimation sample contains the rest of the data.

p = 4; PS = DTT(1:p,:); InSample = DTT((p+1):end,:); respnames = ["CPIAUCSL" "UNRATE" "RGDP"]; idx = endsWith(InSample.Properties.VariableNames,"GCE"); prednames = InSample.Properties.VariableNames(idx);

Create a default VAR(4) model by using the shorthand syntax. Specify the response variable names.

Mdl = varm(3,p); Mdl.SeriesNames = respnames;

Estimate the model using the entire sample. Specify the GCE and its lags as exogenous predictor data for the regression component.

EstMdl = estimate(Mdl,InSample,Presample=PS,PredictorVariables=prednames);

Generate 100 random response and innovations paths from the estimated model by performing an unconditional simulation. Specify that the length of the paths is the same as the length of the estimation sample period. Supply the presample and estimation sample data.

rng(1) % For reproducibility numpaths = 100; numobs = height(InSample); Tbl = simulate(EstMdl,numobs,NumPaths=numpaths, ... Presample=PS,InSample=InSample,PredictorVariables=prednames); size(Tbl)

ans = 1×2

240 14

head(Tbl)

Time CPIAUCSL RGDP GCE UNRATE Lag1GCE Lag2GCE Lag3GCE Lag4GCE CPIAUCSL_Responses UNRATE_Responses RGDP_Responses CPIAUCSL_Innovations UNRATE_Innovations RGDP_Innovations

_____ __________ __________ __________ ______ __________ __________ __________ __________ __________________ ________________ ______________ ____________________ __________________ ________________

Q1-49 0.00041815 -0.0031645 0.036603 6.2 0.047147 0.04948 0.04193 0.054347 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double

Q2-49 -0.0071324 0.011385 -0.0021164 6.6 0.036603 0.047147 0.04948 0.04193 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double

Q3-49 -0.0059122 -0.010366 -0.012793 6.6 -0.0021164 0.036603 0.047147 0.04948 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double

Q4-49 0.0012698 0.040091 -0.021693 6.3 -0.012793 -0.0021164 0.036603 0.047147 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double

Q1-50 0.010101 0.029649 0.010905 5.4 -0.021693 -0.012793 -0.0021164 0.036603 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double

Q2-50 0.01908 0.03844 -0.0043478 4.4 0.010905 -0.021693 -0.012793 -0.0021164 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double

Q3-50 0.025954 0.017994 0.075508 4.3 -0.0043478 0.010905 -0.021693 -0.012793 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double

Q4-50 0.035395 0.01197 0.14807 3.4 0.075508 -0.0043478 0.010905 -0.021693 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double 1x100 double

Tbl is a 240-by-14 timetable of estimation sample data, simulated responses (denoted responseName_Responses), and corresponding innovations (denoted responseName_Innovations). The simulated response and innovations variables are 240-by-100 matrices, where each row is a period in the estimation sample and each column is a separate, independently generated path.

For each time in the estimation sample, compute the mean vector of the simulated responses among all paths.

idx = endsWith(Tbl.Properties.VariableNames,"_Responses");

simrespnames = Tbl.Properties.VariableNames(idx);

MeanSim = varfun(@(x)mean(x,2),Tbl,InputVariables=simrespnames);MeanSim is a 240-by-3 timetable containing the average of the simulated responses at each time point.

Plot the simulated responses, their averages, and the data.

figure tiledlayout(2,2) for j = 1:Mdl.NumSeries nexttile plot(Tbl.Time,Tbl{:,simrespnames(j)},Color=[0.8,0.8,0.8]) title(Mdl.SeriesNames{j}); hold on h1 = plot(Tbl.Time,Tbl{:,respnames(j)}); h2 = plot(Tbl.Time,MeanSim{:,"Fun_"+simrespnames(j)}); hold off end hl = legend([h1 h2],"Data","Mean"); hl.Position = [0.6 0.25 hl.Position(3:4)];

Return Timetable of Responses and Innovations from Conditional Simulation

Since R2022b

Perform a conditional simulation of the VAR model in Return Timetable of Responses and Innovations from Unconditional Simulation, in which economists hypothesize that the unemployment rate is 6% for 15 quarters after the end of the sampling period (from Q2 of 2009 through Q4 of 2012).

Load and Preprocess Data

Load the Data_USEconModel data set. Compute the CPI growth rate. Because the growth rate calculation consumes the earliest observation, include the rate variable in the timetable by prepending the series with NaN.

load Data_USEconModel

DataTimeTable.RCPI = [NaN; price2ret(DataTimeTable.CPIAUCSL)];Prepare Timetable for Estimation

Remove all missing values from the table, relative to the CPI rate (RCPI) and unemployment rate (UNRATE) series.

varnames = ["RCPI" "UNRATE"]; DTT = rmmissing(DataTimeTable,DataVariables=varnames);

Remedy the time irregularity by shifting all dates to the first day of the quarter.

dt = DTT.Time; dt = dateshift(dt,"start","quarter"); DTT.Time = dt;

Create Model Template for Estimation

Create a default VAR(4) model by using the shorthand syntax. Specify the response variable names.

p = 4; Mdl = varm(2,p); Mdl.SeriesNames = varnames;

Fit Model to Data

Estimate the model. Pass the entire timetable DTT. By default, estimate selects the response variables in Mdl.SeriesNames to fit to the model. Alternatively, you can use the ResponseVariables name-value argument.

EstMdl = estimate(Mdl,DTT);

Prepare for Conditional Simulation of Estimated Model

Suppose economists hypothesize that the unemployment rate will be at 6% for the next 15 quarters.

Create a timetable with the following qualities:

The timestamps are regular with respect to the estimation sample timestamps and they are ordered from Q2 of 2009 through Q4 of 2012.

The variable

RCPI(and, consequently, all other variables inDTT) is a 15-by-1 vector ofNaNvalues.The variable

UNRATEis a 15-by-1 vector, where each element is 6.

numobs = 15;

shdt = DTT.Time(end) + calquarters(1:numobs);

DTTCondSim = retime(DTT,shdt,"fillwithmissing");

DTTCondSim.UNRATE = ones(numobs,1)*6;DTTCondSim is a 15-by-15 timetable that follows directly, in time, from DTT, and both timetables have the same variables. All variables in DTTCondSim contain NaN values, except for UNRATE, which is a vector composed of the value 6.

Perform Conditional Simulation of Estimated Model

Simulate the CPI growth rate given the hypothesis by supplying the conditioning data DTTCondSim and specifying the response variable names. Generate 1000 paths. Because the simulation horizon is beyond the estimation sample data, supply the estimation sample as a presample to initialize the model.

rng(1) % For reproducibility Tbl = simulate(EstMdl,numobs,NumPaths=1000, ... InSample=DTTCondSim,ResponseVariables=EstMdl.SeriesNames, ... Presample=DTT,PresampleResponseVariables=EstMdl.SeriesNames); size(Tbl)

ans = 1×2

15 19

idx = endsWith(Tbl.Properties.VariableNames,["_Responses" "_Innovations"]); head(Tbl(:,idx))

Time RCPI_Responses UNRATE_Responses RCPI_Innovations UNRATE_Innovations

_____ ______________ ________________ ________________ __________________

Q2-09 1x1000 double 1x1000 double 1x1000 double 1x1000 double

Q3-09 1x1000 double 1x1000 double 1x1000 double 1x1000 double

Q4-09 1x1000 double 1x1000 double 1x1000 double 1x1000 double

Q1-10 1x1000 double 1x1000 double 1x1000 double 1x1000 double

Q2-10 1x1000 double 1x1000 double 1x1000 double 1x1000 double

Q3-10 1x1000 double 1x1000 double 1x1000 double 1x1000 double

Q4-10 1x1000 double 1x1000 double 1x1000 double 1x1000 double

Q1-11 1x1000 double 1x1000 double 1x1000 double 1x1000 double

Tbl is a 15-by-19 matrix of simulated responses and innovations of RCPI given UNRATE is 6% for the next 15 quarters. RCPI_Responses contains the simulated paths of the CPI growth rate and RCPI_Innovations contains the corresponding innovations series. UNRATE_Responses is a 15-by-1000 matrix composed of the value 6. All other variables in Tbl are the variables and their values in DTTCondSim.

Plot the simulated values of the CPI growth rate and their mean with the final few values of the estimation sample data.

MeanRCPISim = mean(Tbl.RCPI_Responses,2); figure h1 = plot(DTT.Time((end-30):end),DTT.RCPI((end-30):end)); hold on h2 = plot(Tbl.Time,Tbl.RCPI_Responses,Color=[0.8 0.8 0.8]); h3 = plot(Tbl.Time,MeanRCPISim,Color="k",LineWidth=2); xline(Tbl.Time(1),"r--",LineWidth=2) hold off title(EstMdl.SeriesNames) legend([h1 h2(1) h3],["Estimation data" "Simulated paths" "Simulation mean"], ... Location="best")

Input Arguments

Output Arguments

Algorithms

Suppose Y0 and YF are the presample and future

response data specified by the numeric data inputs in Y0 and

YF or the selected variables from the input tables or

timetables Presample and InSample. Similarly,

suppose E contains the simulated model innovations as returned in the

numeric array E or the table or timetable

Tbl.

simulateperforms conditional simulation using this process for all pagesk= 1,...,numpathsand for each timet= 1,...,numobs.simulateinfers (or inverse filters) the model innovations for all response variables (E(from the known future responses (t,:,k)YF(). Int,:,k)E,simulatemimics the pattern ofNaNvalues that appears inYF.For the missing elements of

Eat timet,simulateperforms these steps.Draw

Z1, the random, standard Gaussian distribution disturbances conditional on the known elements ofE.Scale

Z1by the lower triangular Cholesky factor of the conditional covariance matrix. That is,Z2=L*Z1, whereL=chol(C,"lower")andCis the covariance of the conditional Gaussian distribution.Impute

Z2in place of the corresponding missing values inE.

For the missing values in

YF,simulatefilters the corresponding random innovations through the modelMdl.

simulateuses this process to determine the time origin t0 of models that include linear time trends.If you do not specify

Y0, then t0 = 0.Otherwise,

simulatesets t0 tosize(Y0,1)–Mdl.P. Therefore, the times in the trend component are t = t0 + 1, t0 + 2,..., t0 +numobs. This convention is consistent with the default behavior of model estimation in whichestimateremoves the firstMdl.Presponses, reducing the effective sample size. Althoughsimulateexplicitly uses the firstMdl.Ppresample responses inY0to initialize the model, the total number of observations inY0(excluding any missing values) determines t0.

References

[1] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[2] Johansen, S. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models. Oxford: Oxford University Press, 1995.

[3] Juselius, K. The Cointegrated VAR Model. Oxford: Oxford University Press, 2006.

[4] Lütkepohl, H. New Introduction to Multiple Time Series Analysis. Berlin: Springer, 2005.

Version History

Introduced in R2017aYou can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)