vratiotest

Variance ratio test for random walk

Syntax

Description

h = vratiotest(y)

StatTbl = vratiotest(Tbl)DataVariable name-value

argument.

[___] = vratiotest(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)vratiotest returns the output argument combination for the

corresponding input arguments.

Some options control the number of tests to conduct. The following conditions apply when

vratiotest conducts multiple tests:

For example,

vratiotest(Tbl,DataVariable="GDP",Alpha=0.025,IID=[false true])

conducts two tests, at a level of significance of 0.025, on the variable

GDP of the input table. The first test does not assume that the

innovations series is iid and the second test assumes that the innovations series is

iid.

Examples

Conduct Variance Ratio Test on Vector of Data

Test whether a time series is a random walk using the default options of vratiotest. Input the time series data as a numeric vector.

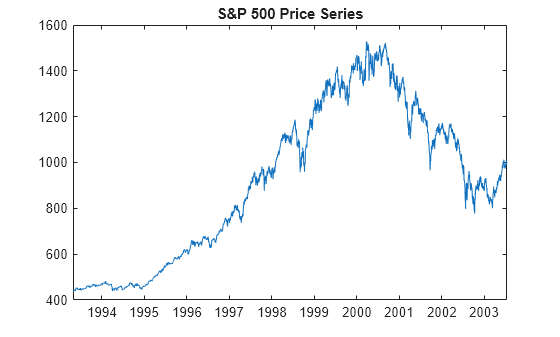

Load the global large-cap equity indices data set, which contains daily closing prices during 1993–2003. Extract the closing prices of the S&P 500 series.

load Data_GlobalIdx1 dt = datetime(dates,ConvertFrom="datenum"); sp = DataTable.SP; plot(dt,sp) title("S&P 500 Price Series")

The first half of the series exhibits exponential growth.

Scale the series by applying the log transformation.

logsp = log(DataTable.SP);

The logsp series is in levels.

Assess the null hypothesis that the log series is a random walk by applying the variance ratio test. Use default options.

h = vratiotest(logsp)

h = logical

0

h = 0 indicates that, at a 5% level of significance, the test fails to reject the null hypothesis that the series is a random walk.

Return Test p-Value and Decision Statistics

Load the global large-cap equity indices data set, extract the closing prices of the S&P 500 price series, and apply the log transform to the series.

load Data_GlobalIdx1

logsp = log(DataTable.SP);Assess the null hypothesis that the log series is a random walk by applying the variance ratio test. Return the test decision, -value, test statistic, and critical value.

[h,pValue,stat,cValue] = vratiotest(logsp)

h = logical

0

pValue = 0.7004

stat = 0.3847

cValue = 1.9600

Conduct Variance Ratio Test on Table Variable

Test whether a time series, which is one variable in a table, is a random walk using the default options.

Load the global large-cap equity indices data set. Convert the table DataTable to a timetable.

load Data_GlobalIdx1 dates = datetime(dates,ConvertFrom="datenum"); TT = table2timetable(DataTable,RowTimes=dates);

Apply the log transform to all series.

LTT = varfun(@log,TT(:,2:end));

LTT.Properties.VariableNames{end}ans = 'log_SP'

The last variable in the table is the log of the S&P 500 price series log_SP.

Assess the null hypothesis of the variance ratio test that the log of the S&P 500 price series is a random walk.

StatTbl = vratiotest(LTT)

StatTbl=1×7 table

h pValue stat cValue Alpha Period IID

_____ _______ _______ ______ _____ ______ _____

Test 1 false 0.70045 0.38471 1.96 0.05 2 false

vratiotest returns test results and settings in the table StatTbl, where variables correspond to test results (h, pValue, stat, and cValue) and settings (Alpha, Period, and IID), and rows correspond to individual tests (in this case, vratiotest conducts one test).

By default, vratiotest tests the last variable in the table. To select a variable from an input table to test, set the DataVariable option.

Adjust Number of Overlapping Periods for Test

Test whether the S&P 500 series is a random walk using various step sizes, with and without the iid innovations assumption.

Load the global large-cap equity indices data set. Convert the table DataTable to a timetable and apply the log transform to all timetable variables.

load Data_GlobalIdx1 dates = datetime(dates,ConvertFrom="datenum"); TT = table2timetable(DataTable,RowTimes=dates); LTT = varfun(@log,TT(:,2:end));

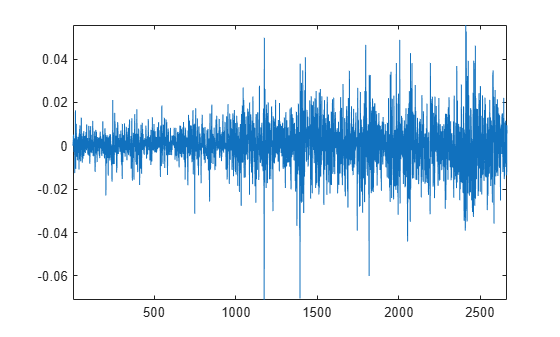

Plot the S&P 500 returns.

plot(diff(LTT.log_SP))

axis tight

The plot indicates that the returns have possible conditional heteroscedasticity.

Conduct separate tests for whether the series is a random walk using periods 2, 4, and 8. For each period, conduct separate tests assuming the innovations are iid and without the assumption. Return the variance ratios of each test, and compute the first-order autocorrelation of the returns from the first ratio.

q = [2 4 8 2 4 8];

iid = logical([1 1 1 0 0 0]);

[StatTbl,ratio] = vratiotest(LTT,Period=q,IID=iid,DataVariable="log_SP")StatTbl=6×7 table

h pValue stat cValue Alpha Period IID

_____ ________ ________ ______ _____ ______ _____

Test 1 false 0.56704 0.57242 1.96 0.05 2 true

Test 2 false 0.33073 -0.97265 1.96 0.05 4 true

Test 3 true 0.030933 -2.1579 1.96 0.05 8 true

Test 4 false 0.70045 0.38471 1.96 0.05 2 false

Test 5 false 0.50788 -0.66214 1.96 0.05 4 false

Test 6 false 0.13034 -1.5128 1.96 0.05 8 false

ratio = 6×1

1.0111

0.9647

0.8763

1.0111

0.9647

0.8763

rho1 = ratio(1) - 1 % First-order autocorrelation of returnsrho1 = 0.0111

StatTbl.h indicates that the test fails to reject that the series is a random walk at 5% level, except in the case where period = 8 and IID = true. This rejection is likely due to the test not accounting for the heteroscedasticity.

Input Arguments

Output Arguments

More About

Tips

The test finds the largest integer n such that nq ≤ T – 1, where q is the vaule of the

Periodargument and T is the sample size. Then, the test discards the final (T–1) – nq observations. To include these final observations, remove the initial (T–1) – nq observations from the input series before you run the test.

References

[1] Campbell, J. Y., A. W. Lo, and A. C. MacKinlay. Chapter 12. “The Econometrics of Financial Markets.” Nonlinearities in Financial Data. Princeton, NJ: Princeton University Press, 1997.

[2] Cecchetti, S. G., and P. S. Lam. “Variance-Ratio Tests: Small-Sample Properties with an Application to International Output Data.” Journal of Business and Economic Statistics. Vol. 12, 1994, pp. 177–186.

[3] Cochrane, J. “How Big is the Random Walk in GNP?” Journal of Political Economy. Vol. 96, 1988, pp. 893–920.

[4] Faust, J. “When Are Variance Ratio Tests for Serial Dependence Optimal?” Econometrica. Vol. 60, 1992, pp. 1215–1226.

[5] Lo, A. W., and A. C. MacKinlay. “Stock Market Prices Do Not Follow Random Walks: Evidence from a Simple Specification Test.” Review of Financial Studies. Vol. 1, 1988, pp. 41–66.

[6] Lo, A. W., and A. C. MacKinlay. “The Size and Power of the Variance Ratio Test.” Journal of Econometrics. Vol. 40, 1989, pp. 203–238.

[7] Lo, A. W., and A. C. MacKinlay. A Non-Random Walk Down Wall St. Princeton, NJ: Princeton University Press, 2001.

Version History

Introduced in R2009b

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)