simulate

Simulate multivariate stochastic differential equations (SDEs) for

SDE, BM, GBM,

CEV, CIR, HWV,

Heston, SDEDDO, SDELD,

SDEMRD, Merton, or Bates

models

Description

[

adds optional inputs for Paths,Times,Z] = simulate(___,Optional,Scheme)Optional and

Scheme.

The Optional input argument for simulate

accepts any variable-length list of input arguments that the simulation method or

function referenced by the SDE.Simulation parameter requires or

accepts. It passes this input list directly to the appropriate SDE simulation method

or user-defined simulation function.

The optional input Scheme lets you specify an approximation

scheme used to simulate the sample paths and you can use this optional input with or

without an Optional input argument.

Examples

Antithetic Sampling to a Path-Dependent Barrier Option

Consider a European up-and-in call option on a single underlying stock. The evolution of this stock's price is governed by a Geometric Brownian Motion (GBM) model with constant parameters:

![]()

Assume the following characteristics:

The stock currently trades at 105.

The stock pays no dividends.

The stock volatility is 30% per annum.

The option strike price is 100.

The option expires in three months.

The option barrier is 120.

The risk-free rate is constant at 5% per annum.

The goal is to simulate various paths of daily stock prices, and calculate the price of the barrier option as the risk-neutral sample average of the discounted terminal option payoff. Since this is a barrier option, you must also determine if and when the barrier is crossed.

This example performs antithetic sampling by explicitly setting the Antithetic flag to true, and then specifies an end-of-period processing function to record the maximum and terminal stock prices on a path-by-path basis.

Create a GBM model using gbm.

barrier = 120; % barrier strike = 100; % exercise price rate = 0.05; % annualized risk-free rate sigma = 0.3; % annualized volatility nPeriods = 63; % 63 trading days dt = 1 / 252; % time increment = 252 days Time = nPeriods * dt; % expiration time = 0.25 years obj = gbm(rate, sigma, 'StartState', 105);

Perform a small-scale simulation that explicitly returns two simulated paths.

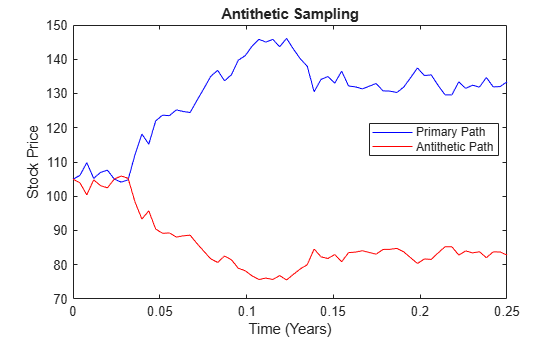

rng('default') % make output reproducible [X, T] = obj.simBySolution(nPeriods, 'DeltaTime', dt, ... 'nTrials', 2, 'Antithetic', true);

Perform antithetic sampling such that all primary and antithetic paths are simulated and stored in successive matching pairs. Odd paths (1,3,5,...) correspond to the primary Gaussian paths. Even paths (2,4,6,...) are the matching antithetic paths of each pair, derived by negating the Gaussian draws of the corresponding primary (odd) path. Verify this by examining the matching paths of the primary/antithetic pair.

plot(T, X(:,:,1), 'blue', T, X(:,:,2), 'red') xlabel('Time (Years)'), ylabel('Stock Price'), ... title('Antithetic Sampling') legend({'Primary Path' 'Antithetic Path'}, ... 'Location', 'Best')

To price the European barrier option, specify an end-of-period processing function to record the maximum and terminal stock prices. This processing function is accessible by time and state, and is implemented as a nested function with access to shared information that allows the option price and corresponding standard error to be calculated. For more information on using an end-of-period processing function, see Pricing Equity Options.

Simulate 200 paths using the processing function method.

rng('default') % make output reproducible barrier = 120; % barrier strike = 100; % exercise price rate = 0.05; % annualized risk-free rate sigma = 0.3; % annualized volatility nPeriods = 63; % 63 trading days dt = 1 / 252; % time increment = 252 days Time = nPeriods * dt; % expiration time = 0.25 years obj = gbm(rate, sigma, 'StartState', 105); nPaths = 200; % # of paths = 100 sets of pairs f = Example_BarrierOption(nPeriods, nPaths); simulate(obj, nPeriods, 'DeltaTime' , dt, ... 'nTrials', nPaths, 'Antithetic', true, ... 'Processes', f.SaveMaxLast);

Approximate the option price with a 95% confidence interval.

optionPrice = f.OptionPrice(strike, rate, barrier);

standardError = f.StandardError(strike, rate, barrier,...

true);

lowerBound = optionPrice - 1.96 * standardError;

upperBound = optionPrice + 1.96 * standardError;

displaySummary(optionPrice, standardError, lowerBound, upperBound); Up-and-In Barrier Option Price: 6.6572

Standard Error of Price: 0.7292

Confidence Interval Lower Bound: 5.2280

Confidence Interval Upper Bound: 8.0864

Utility Function

function displaySummary(optionPrice, standardError, lowerBound, upperBound) fprintf(' Up-and-In Barrier Option Price: %8.4f\n', ... optionPrice); fprintf(' Standard Error of Price: %8.4f\n', ... standardError); fprintf(' Confidence Interval Lower Bound: %8.4f\n', ... lowerBound); fprintf(' Confidence Interval Upper Bound: %8.4f\n', ... upperBound); end

Specify Approximation Scheme with simulate Using a CIR Model

The Cox-Ingersoll-Ross (CIR) short rate class derives directly from SDE with mean-reverting drift (SDEMRD):

where is a diagonal matrix whose elements are the square root of the corresponding element of the state vector.

Create a cir object to represent the model: .

cir_obj = cir(0.2, 0.1, 0.05) % (Speed, Level, Sigma)cir_obj =

Class CIR: Cox-Ingersoll-Ross

----------------------------------------

Dimensions: State = 1, Brownian = 1

----------------------------------------

StartTime: 0

StartState: 1

Correlation: 1

Drift: drift rate function F(t,X(t))

Diffusion: diffusion rate function G(t,X(t))

Simulation: simulation method/function simByEuler

Sigma: 0.05

Level: 0.1

Speed: 0.2

Use the optional name-value argument for 'Scheme' to specify a scheme to simulate the sample paths.

[paths,times] = simulate(cir_obj,10,'ntrials',4096,'scheme','quadratic-exponential');

Use simulate with Quasi-Monte Carlo Simulation with simByEuler Using a CIR Model

The Cox-Ingersoll-Ross (CIR) short rate class derives directly from SDE with mean-reverting drift (SDEMRD):

where is a diagonal matrix whose elements are the square root of the corresponding element of the state vector.

Create a cir object to represent the model: .

cir_obj = cir(0.2, 0.1, 0.05) % (Speed, Level, Sigma)cir_obj =

Class CIR: Cox-Ingersoll-Ross

----------------------------------------

Dimensions: State = 1, Brownian = 1

----------------------------------------

StartTime: 0

StartState: 1

Correlation: 1

Drift: drift rate function F(t,X(t))

Diffusion: diffusion rate function G(t,X(t))

Simulation: simulation method/function simByEuler

Sigma: 0.05

Level: 0.1

Speed: 0.2

Use optional name-value inputs for the simByEuler method that you can call through simulate interface using the simulate 'Scheme' for 'quadratic-exponential'. The optional inputs for simByEuler define a quasi-Monte Carlo simulation using the name-value arguments for 'MonteCarloMethod','QuasiSequence', and 'BrownianMotionMethod'.

[paths,time] = simulate(cir_obj,10,'ntrials',4096,'montecarlomethod','quasi','quasisequence','sobol','BrownianMotionMethod','brownian-bridge','scheme','quadratic-exponential');

Use simulate with Quasi-Monte Carlo Simulation with simByMilstein Using a CIR Model

The Cox-Ingersoll-Ross (CIR) short rate class derives directly from SDE with mean-reverting drift (SDEMRD):

where is a diagonal matrix whose elements are the square root of the corresponding element of the state vector.

Create a cir object to represent the model: .

cir_obj = cir(0.2, 0.1, 0.05) % (Speed, Level, Sigma)cir_obj =

Class CIR: Cox-Ingersoll-Ross

----------------------------------------

Dimensions: State = 1, Brownian = 1

----------------------------------------

StartTime: 0

StartState: 1

Correlation: 1

Drift: drift rate function F(t,X(t))

Diffusion: diffusion rate function G(t,X(t))

Simulation: simulation method/function simByEuler

Sigma: 0.05

Level: 0.1

Speed: 0.2

Use optional name-value inputs for the simByMilstein method that you can call through simulate interface using the simulate 'Scheme' for 'milstein'. The optional inputs for simByMilstein define a quasi-Monte Carlo simulation using the name-value arguments for 'MonteCarloMethod','QuasiSequence', and 'BrownianMotionMethod'.

[paths,time] = simulate(cir_obj,10,'ntrials',4096,'montecarlomethod','quasi','quasisequence','sobol','BrownianMotionMethod','brownian-bridge','scheme','milstein');

Use simulate with Quasi-Monte Carlo Simulation with simByMilstein2 Using a CIR Model

The Cox-Ingersoll-Ross (CIR) short rate class derives directly from SDE with mean-reverting drift (SDEMRD):

where is a diagonal matrix whose elements are the square root of the corresponding element of the state vector.

Create a cir object to represent the model: .

cir_obj = cir(0.2, 0.1, 0.05) % (Speed, Level, Sigma)cir_obj =

Class CIR: Cox-Ingersoll-Ross

----------------------------------------

Dimensions: State = 1, Brownian = 1

----------------------------------------

StartTime: 0

StartState: 1

Correlation: 1

Drift: drift rate function F(t,X(t))

Diffusion: diffusion rate function G(t,X(t))

Simulation: simulation method/function simByEuler

Sigma: 0.05

Level: 0.1

Speed: 0.2

Use optional name-value inputs for the simByMilstein2 method that you can call through simulate interface using the simulate 'Scheme' for 'milstein2'. The optional inputs for simByMilstein2 define a quasi-Monte Carlo simulation using the name-value arguments for 'MonteCarloMethod','QuasiSequence', and 'BrownianMotionMethod'.

[paths,time] = simulate(cir_obj,10,'ntrials',4096,'montecarlomethod','quasi','quasisequence','sobol','BrownianMotionMethod','brownian-bridge','scheme','milstein2');

Input Arguments

Output Arguments

More About

Algorithms

This function simulates any vector-valued SDE of the form:

| (1) |

X is an NVars-by-

1state vector of process variables (for example, short rates or equity prices) to simulate.W is an NBrowns-by-

1Brownian motion vector.F is an NVars-by-

1vector-valued drift-rate function.G is an NVars-by-NBrowns matrix-valued diffusion-rate function.

References

[1] Ait-Sahalia, Y. “Testing Continuous-Time Models of the Spot Interest Rate.” The Review of Financial Studies, Spring 1996, Vol. 9, No. 2, pp. 385–426.

[2] Ait-Sahalia, Y. “Transition Densities for Interest Rate and Other Nonlinear Diffusions.” The Journal of Finance, Vol. 54, No. 4, August 1999.

[3] Glasserman, P. Monte Carlo Methods in Financial Engineering, New York, Springer-Verlag, 2004.

[4] Hull, J. C. Options, Futures, and Other Derivatives, 5th ed. Englewood Cliffs, NJ: Prentice Hall, 2002.

[5] Johnson, N. L., S. Kotz, and N. Balakrishnan. Continuous Univariate Distributions, Vol. 2, 2nd ed. New York, John Wiley & Sons, 1995.

[6] Shreve, S. E. Stochastic Calculus for Finance II: Continuous-Time Models, New York: Springer-Verlag, 2004.

Version History

Introduced in R2008aSee Also

simByEuler | simBySolution | simBySolution | sde | merton | bates | bm | gbm | sdeddo | sdeld | cev | cir | heston | hwv | sdemrd | simByMilstein2 | simByMilstein2 | simByMilstein2 | simByMilstein2 | simByMilstein2 | simByMilstein | simByMilstein | simByMilstein | simByMilstein | simByMilstein

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)