bootstrap

Bootstrap interest-rate curve from market data

Syntax

Description

DCurve = IRDataCurve.bootstrap(Type,Settle,InstrumentTypes,Instruments)

Note

The ratecurve object and associated

methods were introduced in R2020a as part of a new object-based framework in the

Financial Instruments Toolbox™ which supports end-to-end workflows in instrument modeling and analysis.

For more information, see irbootstrap and Get Started with Workflows Using Object-Based Framework for Pricing Financial Instruments.

DCurve = IRDataCurve.bootstrap(___,Name,Value)

Examples

Use the bootstrap Method to Create an IRDataCurve Object

In this bootstrapping example, InstrumentTypes, Instruments, and a Settle date are defined:

InstrumentTypes = {'Deposit';'Deposit';...

'Futures';'Futures';'Futures';'Futures';'Futures';'Futures';...

'Swap';'Swap';'Swap';'Swap';};

Instruments = [datenum('08/10/2007'),datenum('09/17/2007'),.0532000; ...

datenum('08/10/2007'),datenum('11/17/2007'),.0535866; ...

datenum('08/08/2007'),datenum('19-Dec-2007'),9485; ...

datenum('08/08/2007'),datenum('19-Mar-2008'),9502; ...

datenum('08/08/2007'),datenum('18-Jun-2008'),9509.5; ...

datenum('08/08/2007'),datenum('17-Sep-2008'),9509; ...

datenum('08/08/2007'),datenum('17-Dec-2008'),9505.5; ...

datenum('08/08/2007'),datenum('18-Mar-2009'),9501; ...

datenum('08/08/2007'),datenum('08/08/2014'),.0530; ...

datenum('08/08/2007'),datenum('08/08/2019'),.0551; ...

datenum('08/08/2007'),datenum('08/08/2027'),.0565; ...

datenum('08/08/2007'),datenum('08/08/2037'),.0566];

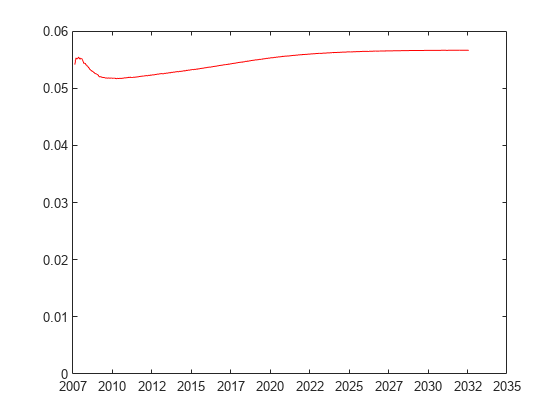

CurveSettle = datenum('08/10/2007');Use the bootstrap method to create an IRDataCurve object.

bootModel = IRDataCurve.bootstrap('Forward', CurveSettle, ... InstrumentTypes, Instruments,'InterpMethod','pchip');

To create the plot for the bootstrapped market data:

PlottingDates = (datenum('08/11/2007'):30:CurveSettle+365*25)'; plot(PlottingDates, getParYields(bootModel, PlottingDates),'r') ylim([0 .06]) datetick

Use the bootstrap Method to Create an IRDataCurve Object That Includes Bonds

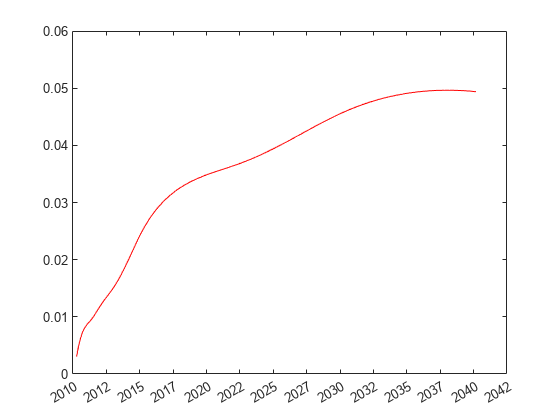

In this bootstrapping example, InstrumentTypes, Instruments, and a Settle date are defined:

CurveSettle = datenum('8-Mar-2010'); InstrumentTypes = {'Deposit';'Deposit';'Deposit';'Deposit';... 'Futures';'Futures';'Futures';'Futures';'Swap';'Swap';'Bond';'Bond'}; Instruments = [datenum('8-Mar-2010'),datenum('8-Apr-2010'),.003; ... datenum('8-Mar-2010'),datenum('8-Jun-2010'),.005; ... datenum('8-Mar-2010'),datenum('8-Sep-2010'),.007; ... datenum('8-Mar-2010'),datenum('8-Mar-2011'),.009; ... datenum('8-Mar-2010'),datenum('18-Jun-2011'),9840; ... datenum('8-Mar-2010'),datenum('17-Sep-2011'),9820; ... datenum('8-Mar-2010'),datenum('17-Dec-2011'),9810; ... datenum('8-Mar-2010'),datenum('18-Mar-2012'),9800; ... datenum('8-Mar-2010'),datenum('8-Mar-2015'),.025; ... datenum('8-Mar-2010'),datenum('8-Mar-2020'),.035; ... datenum('8-Mar-2010'),datenum('8-Mar-2030'),99; ... datenum('8-Mar-2010'),datenum('8-Mar-2040'),101];

When bonds are used, InstrumentCouponRate must be specified:

InstrumentCouponRate = [zeros(10,1);.045;.05];

Note, for parameters that are only applicable to bonds (InstrumentFirstCouponDate, InstrumentLastCouponDate, InstrumentIssueDate, InstrumentFace) the entries for non-bond instruments (deposits and futures) are ignored.

Use the bootstrap method to create an IRDataCurve object.

bootModel = IRDataCurve.bootstrap('Forward', CurveSettle, ... InstrumentTypes, Instruments,'InterpMethod','pchip',... 'InstrumentCouponRate',InstrumentCouponRate);

Create the plot for the bootstrapped market data.

PlottingDates = datemnth(CurveSettle,1:30*12);

plot(PlottingDates, getParYields(bootModel, PlottingDates),'r')

ylim([0 .06])

datetick

Use IRBootstrapOptionsObj with bootstrap for Negative Zero Interest-Rates

Use the IRBootstrapOptionsObj optional argument with the bootstrap method to allow for negative zero rates when solving for the swap zero points.

Settle = datenum('15-Mar-2015'); InstrumentTypes = {'Deposit';'Deposit';'Swap';'Swap';'Swap';'Swap';}; Instruments = [Settle,datenum('15-Jun-2015'),.001; ... Settle,datenum('15-Dec-2015'),.0005; ... Settle,datenum('15-Mar-2016'),-.001; ... Settle,datenum('15-Mar-2017'),-0.0005; ... Settle,datenum('15-Mar-2018'),.0017; ... Settle,datenum('15-Mar-2020'),.0019]; irbo = IRBootstrapOptions('LowerBound',-1); bootModel = IRDataCurve.bootstrap('zero', Settle, InstrumentTypes,... Instruments,'IRBootstrapOptions',irbo); bootModel.getZeroRates(datemnth(Settle,1:60))

ans = 60×1

0.0012

0.0011

0.0010

0.0009

0.0008

0.0008

0.0007

0.0006

0.0005

-0.0000

⋮

Note that optional argument for LowerBound is set to -1 for negative zero rates when solving the swap zero points.

Input Arguments

Output Arguments

Version History

Introduced in R2008b

See Also

IRDataCurve | IRBootstrapOptions | toRateSpec | getForwardRates | getZeroRates | getDiscountFactors | getParYields | irbootstrap

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)