floatbyzero

Price floating-rate note from set of zero curves

Syntax

Description

[ prices

a floating-rate note from a set of zero curves.Price,DirtyPrice,CFlowAmounts,CFlowDates]

= floatbyzero(RateSpec,Spread,Settle,Maturity)

floatbyzero computes prices of vanilla floating-rate

notes and amortizing floating-rate notes.

Note

Alternatively, you can use the FloatBond object to

price floating-rate bond instruments. For more information, see Get Started with Workflows Using Object-Based Framework for Pricing Financial Instruments.

[ adds

additional name-value pair arguments.Price,DirtyPrice,CFlowAmounts,CFlowDates]

= floatbyzero(___,Name,Value)

Examples

Price a Floating-Rate Note Using a Set of Zero Curves

Price a 20-basis point floating-rate note using a set of zero curves.

Load deriv.mat, which provides ZeroRateSpec, the interest-rate term structure, needed to price the bond.

load deriv.mat;Define the floating-rate note using the required arguments. Other arguments use defaults.

Spread = 20; Settle = datetime(2000,1,1); Maturity = datetime(2003,1,1);

Use floatbyzero to compute the price of the note.

Price = floatbyzero(ZeroRateSpec, Spread, Settle, Maturity)

Price = 100.5529

Price an Amortizing Floating-Rate Note

Price an amortizing floating-rate note using the Principal input argument to define the amortization schedule.

Create the RateSpec.

Rates = [0.03583; 0.042147; 0.047345; 0.052707; 0.054302]; ValuationDate = datetime(2011,11,15); StartDates = ValuationDate; EndDates = [datetime(2012,11,15) ; datetime(2013,11,15) ; datetime(2014,11,15) ; datetime(2015,11,15) ; datetime(2016,11,15)]; Compounding = 1; RateSpec = intenvset('ValuationDate', ValuationDate,'StartDates', StartDates,... 'EndDates', EndDates,'Rates', Rates, 'Compounding', Compounding)

RateSpec = struct with fields:

FinObj: 'RateSpec'

Compounding: 1

Disc: [5x1 double]

Rates: [5x1 double]

EndTimes: [5x1 double]

StartTimes: [5x1 double]

EndDates: [5x1 double]

StartDates: 734822

ValuationDate: 734822

Basis: 0

EndMonthRule: 1

Create the floating-rate instrument using the following data:

Settle = datetime(2011,11,15); Maturity = datetime(2015,11,15); Spread = 15;

Define the floating-rate note amortizing schedule.

Principal ={{datetime(2012,11,15) 100;datetime(2013,11,15) 70;datetime(2014,11,15) 40;datetime(2015,11,15) 10}};Compute the price of the amortizing floating-rate note.

Price = floatbyzero(RateSpec, Spread, Settle, Maturity, 'Principal', Principal)Price = 100.3059

Specify the Rate at the Instrument’s Starting Date When It Cannot Be Obtained from the RateSpec

If Settle is not on a reset date of a floating-rate note,

floatbyzero attempts to obtain the latest floating rate before

Settle from RateSpec or the

LatestFloatingRate parameter. When the reset date for this rate is

out of the range of RateSpec (and LatestFloatingRate

is not specified), floatbyzero fails to obtain the rate for that date

and generates an error. This example shows how to use the

LatestFloatingRate input parameter to avoid the error.

Create the error condition when a floating-rate instrument’s StartDate cannot

be determined from the RateSpec.

load deriv.mat;

Spread = 20;

Settle = datetime(2000,1,1);

Maturity = datetime(2003,12,1);

Price = floatbyzero(ZeroRateSpec, Spread, Settle, Maturity)Error using floatbyzero (line 256) The rate at the instrument starting date cannot be obtained from RateSpec. Its reset date (01-Dec-1999) is out of the range of dates contained in RateSpec. This rate is required to calculate cash flows at the instrument starting date. Consider specifying this rate with the 'LatestFloatingRate' input parameter.

Here, the reset date for the rate at Settle was

01-Dec-1999, which was earlier than the valuation date of ZeroRateSpec (01-Jan-2000).

This error can be avoided by specifying the rate at the instrument’s

starting date using the LatestFloatingRate name-value

pair argument.

Define LatestFloatingRate and calculate

the floating-rate price.

Price = floatbyzero(ZeroRateSpec, Spread, Settle, Maturity, 'LatestFloatingRate', 0.03)Price = 100.0285

Price a Floating-Rate Note Using a Different Curve to Generate Floating Cash Flows

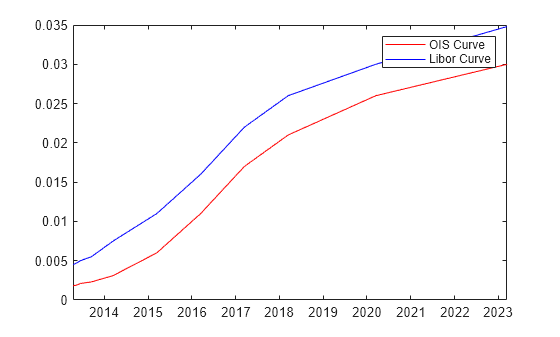

Define the OIS and Libor rates.

Settle = datetime(2013,3,15); CurveDates = daysadd(Settle,360*[1/12 2/12 3/12 6/12 1 2 3 4 5 7 10],1); OISRates = [.0018 .0019 .0021 .0023 .0031 .006 .011 .017 .021 .026 .03]'; LiborRates = [.0045 .0047 .005 .0055 .0075 .011 .016 .022 .026 .030 .0348]';

Plot the dual curves.

figure,plot(CurveDates,OISRates,'r');hold on;plot(CurveDates,LiborRates,'b') legend({'OIS Curve', 'Libor Curve'})

Create an associated RateSpec for the OIS and Libor curves.

OISCurve = intenvset('Rates',OISRates,'StartDate',Settle,'EndDates',CurveDates); LiborCurve = intenvset('Rates',LiborRates,'StartDate',Settle,'EndDates',CurveDates);

Define the floating-rate note.

Maturity = datetime(2018,3,15);

Compute the price for the floating-rate note. The LiborCurve term structure will be used to generate the floating cash flows of the floater instrument. The OISCurve term structure will be used for discounting the cash flows.

Price = floatbyzero(OISCurve,0,Settle,Maturity,'ProjectionCurve',LiborCurve)Price = 102.4214

Some instruments require using different interest-rate curves for generating the floating cash flows and discounting. This is when the ProjectionCurve parameter is useful. When you provide both RateSpec and ProjectionCurve, floatbyzero uses the RateSpec for the purpose of discounting and it uses the ProjectionCurve for generating the floating cash flows.

Input Arguments

Output Arguments

More About

Version History

Introduced before R2006aSee Also

bondbyzero | cfbyzero | fixedbyzero | swapbyzero | intenvset | FloatBond

Topics

- Pricing Using Interest-Rate Term Structure

- Price Portfolio of Bond and Bond Option Instruments

- Compute LIBOR Fallback

- Floating-Rate Note

- Understanding Interest-Rate Tree Models

- Supported Interest-Rate Instrument Functions

- Mapping Financial Instruments Toolbox Functions for Interest-Rate Instrument Objects

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)