spreadsensbyfd

Calculate price and sensitivities of European or American spread options using finite difference method

Syntax

Description

PriceSens = spreadsensbyfd(RateSpec,StockSpec1,StockSpec2,Settle,Maturity,OptSpec,Strike,Corr)StockSpec1 minus the asset defined in

StockSpec2.

PriceSens = spreadsensbyfd(___,Name,Value)

[

returns the PriceSens,PriceGrid,AssetPrice1,AssetPrice2,Times]

= spreadsensbyfd(RateSpec,StockSpec1,StockSpec2,Settle,Maturity,OptSpec,Strike,Corr)PriceSens, PriceGrid,

AssetPrice1, AssetPrice2, and

Times for European or American call or put spread options using the

Alternate Direction Implicit (ADI) finite difference method. The spread is between the

asset defined in StockSpec1 minus the asset defined in

StockSpec2.

[

returns the PriceSens,PriceGrid,AssetPrice1,AssetPrice2,Times]

= spreadsensbyfd(___,Name,Value)PriceSens, PriceGrid,

AssetPrice1, AssetPrice2, and

Times and adds optional name-value pair arguments.

Examples

Compute the Price of a Spread Option Using the Alternate Direction Implicit (ADI) Finite Difference Method

Define the spread option dates.

Settle = datetime(2012,6,1); Maturity = datetime(2012,9,1);

Define asset 1. Price and volatility of RBOB gasoline

Price1gallon = 2.85; % $/gallon Price1 = Price1gallon * 42; % $/barrel Vol1 = 0.29;

Define asset 2. Price and volatility of WTI crude oil

Price2 = 93.20; % $/barrel

Vol2 = 0.36;Define the correlation between the underlying asset prices of asset 1 and asset 2.

Corr = 0.42;

Define the spread option.

OptSpec = 'call';

Strike = 20;Define the RateSpec.

rates = 0.05; Compounding = -1; Basis = 1; RateSpec = intenvset('ValuationDate', Settle, 'StartDates', Settle, ... 'EndDates', Maturity, 'Rates', rates, ... 'Compounding', Compounding, 'Basis', Basis)

RateSpec = struct with fields:

FinObj: 'RateSpec'

Compounding: -1

Disc: 0.9876

Rates: 0.0500

EndTimes: 0.2500

StartTimes: 0

EndDates: 735113

StartDates: 735021

ValuationDate: 735021

Basis: 1

EndMonthRule: 1

Define the StockSpec for the two assets.

StockSpec1 = stockspec(Vol1, Price1)

StockSpec1 = struct with fields:

FinObj: 'StockSpec'

Sigma: 0.2900

AssetPrice: 119.7000

DividendType: []

DividendAmounts: 0

ExDividendDates: []

StockSpec2 = stockspec(Vol2, Price2)

StockSpec2 = struct with fields:

FinObj: 'StockSpec'

Sigma: 0.3600

AssetPrice: 93.2000

DividendType: []

DividendAmounts: 0

ExDividendDates: []

Compute the spread option price and sensitivities based on the Alternate Direction Implicit (ADI) finite difference method.

OutSpec = {'Price', 'Delta', 'Gamma'};

[Price, Delta, Gamma, PriceGrid, AssetPrice1, AssetPrice2, Times] = ...

spreadsensbyfd(RateSpec, StockSpec1, StockSpec2, Settle, ...

Maturity, OptSpec, Strike, Corr, 'OutSpec', OutSpec);Display the price and sensitivities.

Price

Price = 11.1998

Delta

Delta = 1×2

0.6736 -0.6082

Gamma

Gamma = 1×2

0.0190 0.0214

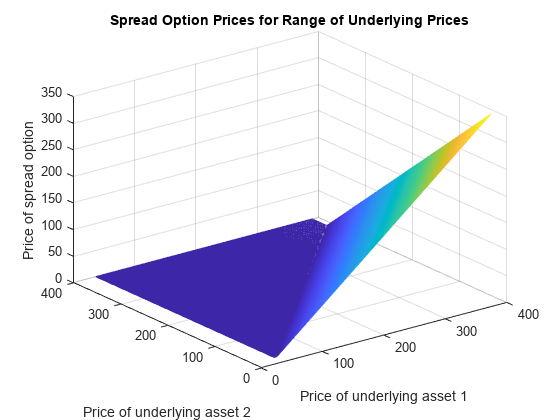

Plot the finite difference grid.

mesh(AssetPrice1, AssetPrice2, PriceGrid(:, :, 1)');

title('Spread Option Prices for Range of Underlying Prices');

xlabel('Price of underlying asset 1');

ylabel('Price of underlying asset 2');

zlabel('Price of spread option');

Input Arguments

Output Arguments

More About

References

[1] Carmona, R., Durrleman, V. “Pricing and Hedging Spread Options.” SIAM Review. Vol. 45, No. 4, pp. 627–685, Society for Industrial and Applied Mathematics, 2003.

[2] Villeneuve, S., Zanette, A. “Parabolic ADI Methods for Pricing American Options on Two Stocks.” Mathematics of Operations Research. Vol. 27, No. 1, pp. 121–149, INFORMS, 2002.

[3] Ikonen, S., Toivanen, J. Efficient Numerical Methods for Pricing American Options Under Stochastic Volatility. Wiley InterScience, 2007.

Version History

Introduced in R2013bYou can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)