Prepayment Risk

Prepayment risk is the risk that the term of the security varies according to differing rates of repayment of principal by borrowers (repayments from refinancings, sales, curtailments, or foreclosures). In a CMO, you can structure the principal (and associated coupon) stream from the underlying mortgage pool collateral to allocate prepayment risk. If principal is prepaid faster than expected (for example, if mortgage rates fall and borrowers refinance), then the overall term of the mortgage pool collateral shortens.

You cannot remove prepayment risk, but you can reallocate it among CMO tranches so that some tranches have some protection against this risk, and other tranches will absorb more of this risk. To facilitate this allocation of prepayment risk, CMOs are structured such that prepayments are allocated among tranches using a fixed set of rules. The most common schemes for prepayment tranching are:

Sequential tranching, with or without, Z-bond tranching

Schedule bond tranching

Planned amortization class (PAC) bonds

Target amortization class (TAC) bonds

Financial Instruments Toolbox™ supports these schemes for prepayment tranching for CMOs and tools for pricing and scheduling cash flows between the tranches, as well as analyzing the price and yield for CMOs. Financial Instruments Toolbox functionality for CMOs does not model credit risk. Therefore, this functionality is most appropriate for CMOs where credit risk is not an issue (for example, agency CMOs where the underlying mortgage pool collateral is insured for default by the agency Government-Sponsored Enterprises (GSEs), such as Fannie Mae and Freddie Mac).

Sequential Tranches Without a Z-Bond

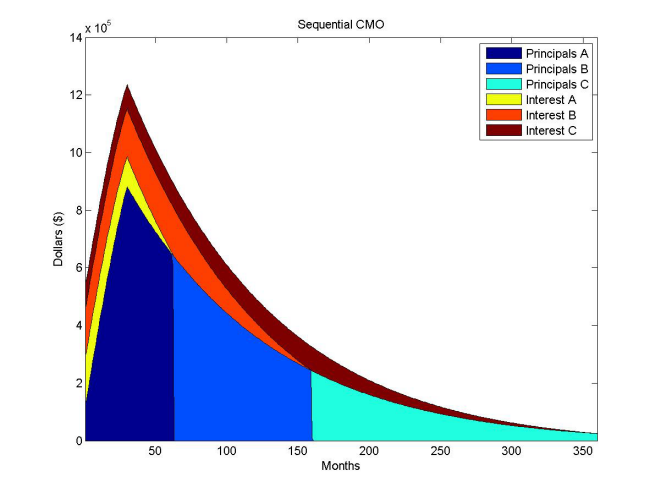

All available principal and interest payments go to the first sequential tranche, until its balance decrements to zero, then to the second, and so on. For example, consider the following example where all principal and interest from the underlying mortgage pool is repaid on tranche A first, then tranche B, then tranche C. Interest is paid on each tranche as long as the principal for the tranche has not been retired.

Sequential Tranches with a Z-Bond

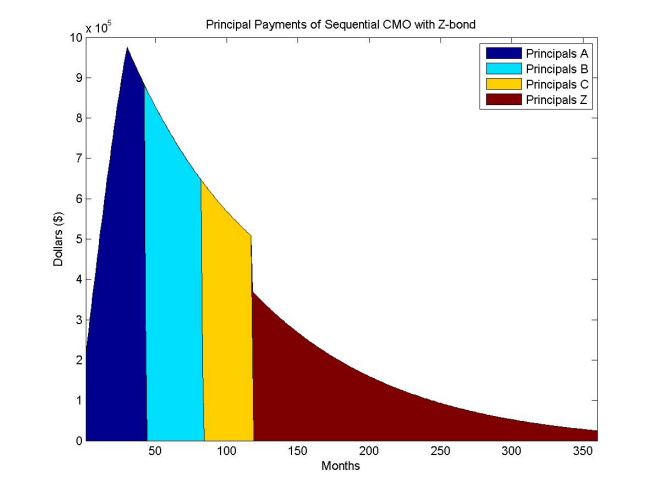

The Z-bond, also called an accrual bond, is a type of interest and principal pay rule. The Z-bond tranche supports other sequential pay tranches by not receiving an interest payment. The interest payment that would have accrued to the Z-bond tranche pays off the principal of other bonds, and the principal of the Z-bond tranche increases. The Z-bond tranche starts receiving interest and principal payments only after the other tranches in the CMO have been fully paid. The Z-bond tranche is used in a sequential-pay structure to accelerate the principal repayments of the sequential-pay bonds.

A Z-bond differs from other CMO instruments because it is not tranching principal but interest. The Z-bond receives no cash flows until all other securities have been paid off. In the interim, the interest that is owed to the Z-bond is accrued to its principal. The following chart demonstrates the difference between a Z-bond and a normal sequential pay tranche. The C tranche pays off sooner with the Z-bond, because the interest cash flows to the Z-bond are being used to pay down the principal of the C tranche.

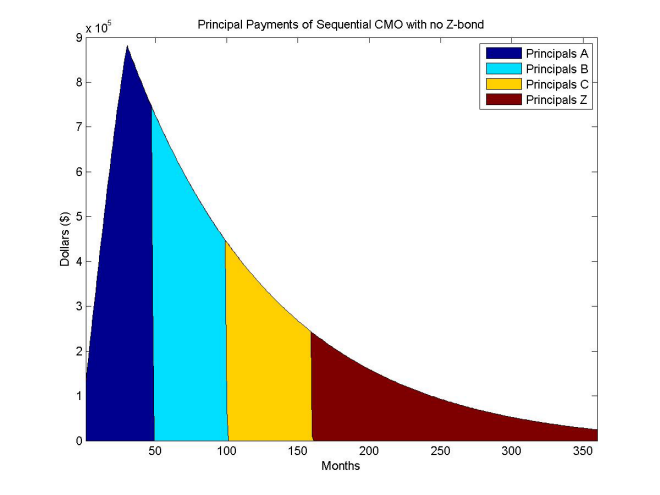

For comparison, the following graphic is the same sequential CMO with no Z-bond.

PAC Tranches

Planned amortization class (PAC) bonds help reduce the effects of prepayment risk. They are designed to produce more stable cash flows by redirecting prepayments from the underlying mortgage collateral to other classes (tranches) called companion or support classes. PAC bonds have a principal payment rate over a predetermined period of time. The PAC bond payment schedule is determined by two different prepayment rates, which together form a band (also called a collar). Early in the life of the CMO, the prepayment at the lower PSA yields a lower prepayment. Later in its life, the principal in the higher PSA declines enough that it yields a lower prepayment. The PAC tranche receives whichever rate is lower, so it will change prepayment at one PSA for the first part of its life, then switch to the other rate. The ability to stay on this schedule is maintained by a support bond, which absorbs excess prepayments, and receives fewer prepayments to prevent extension of average life.

However, the PAC is only protected from extension to the amount that prepayments are made on the underlying MBSs. If there is a sustained period of fast prepayments, then that might completely eliminate a PAC bond’s outstanding support class. When the principal of the associated PAC bond is exhausted, the CMO is called a “busted PAC”, or “busted collar”. Alternatively, in times of slow prepayments, amortization of the support bonds is delayed if there is not enough principal for the currently paying PAC bond. This extends the average life of the class.

A PAC bond protects against both extension and contraction risk by:

Specifying a schedule of principal payments for the PAC bond

Including support tranches that are allocated prepayments inside a specified prepayment band

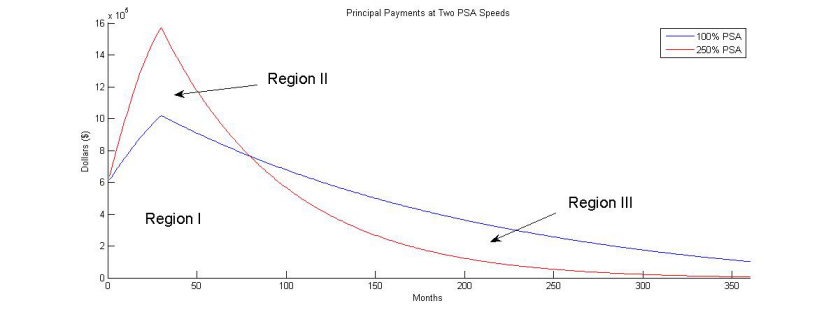

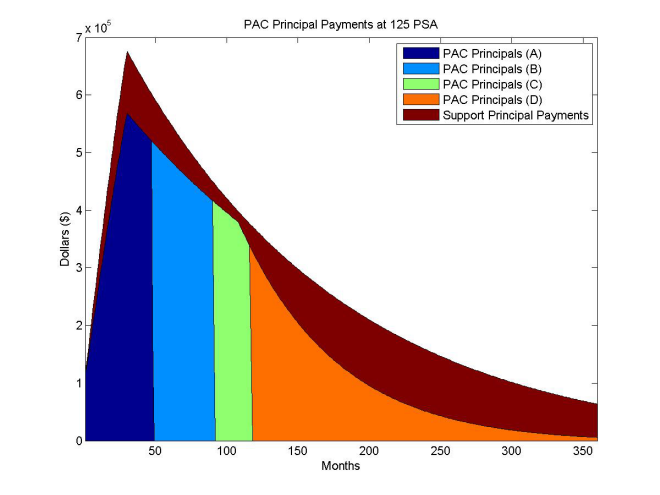

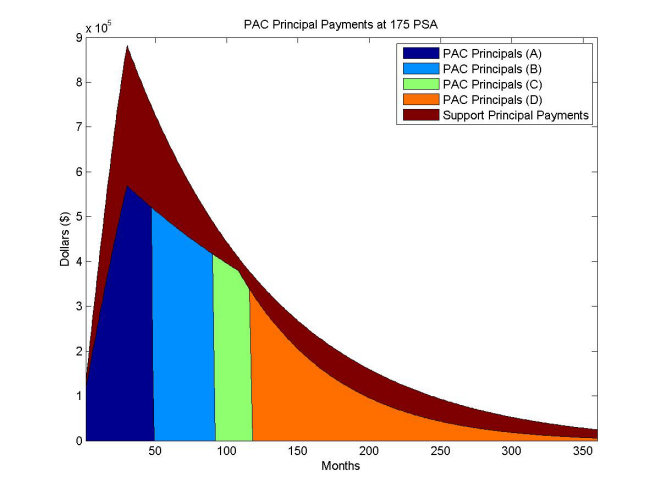

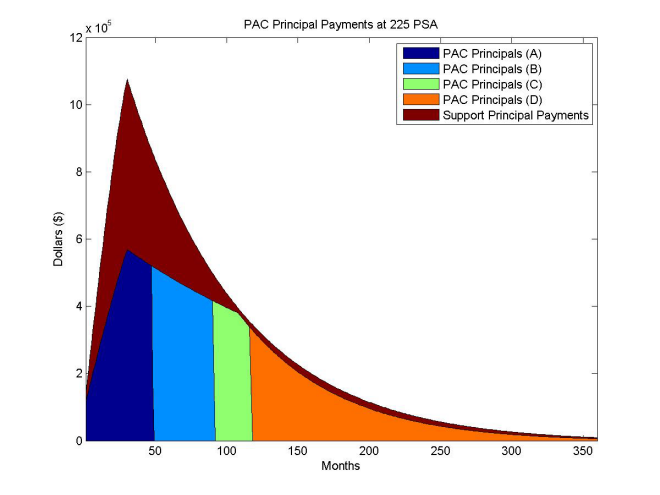

PAC bonds typically specify a band expressed using the PSA model. A PAC bond with a range of 100–250% has this principal schedule.

The principal repayment schedule is the minimum principal payment as Region 1 shows. This is the principal payment schedule as long as the actual prepayment stays within the prepayment band of 100–250% PSA.

For example, for different prepayment speeds of 125%, 175%, and 225% PSA, the actual principal payments are shown in the following graphs. At higher prepayment speeds, the support tranche is allocated principal earlier while the principal timing for the other tranches remains constant.

TAC Tranches

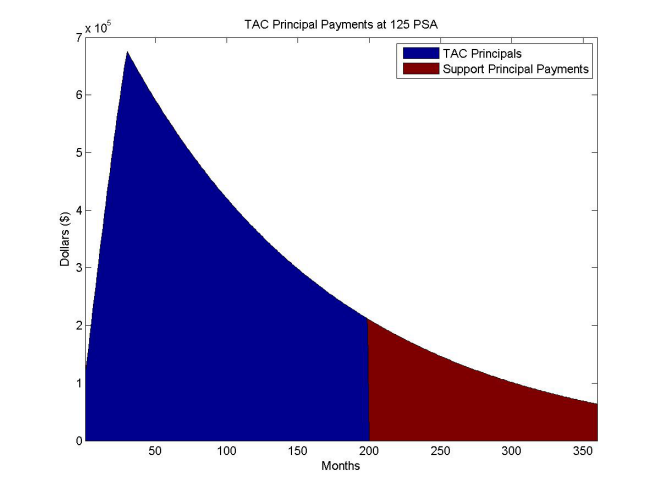

Target amortization class (TAC) bonds are similar to PAC bonds, but they do not provide protection against extension of average life. Create the schedule of principal payments by using just a single PSA. TAC bonds pay a “targeted” principal payment schedule at a single, constant prepayment speed. As long as the underlying mortgage collateral does not prepay at a rate slower than this speed, the TAC bond payment schedule is met. TAC bonds can protect against increasing prepayments and early retirement of the TAC bond investment. If the principal cash flow from the mortgage collateral exceeds the TAC schedule, the excess is allocated to TAC companion (support) classes. Alternatively, if prepayments fall below the speed necessary to maintain the TAC schedule, the weighted average life of the TAC is extended. The TAC bond does not protect against low prepayment rates.

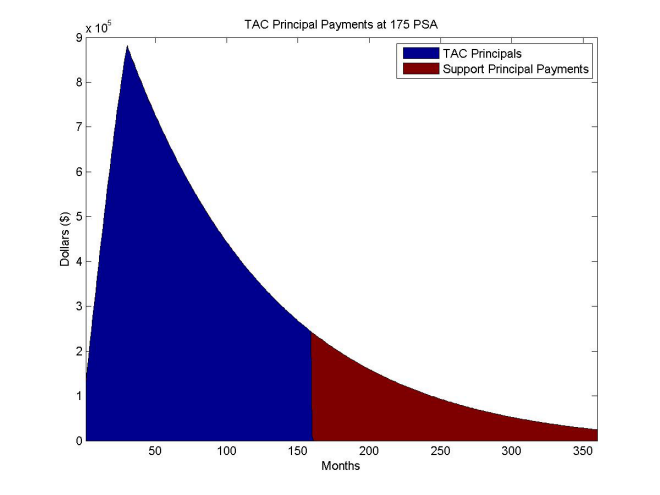

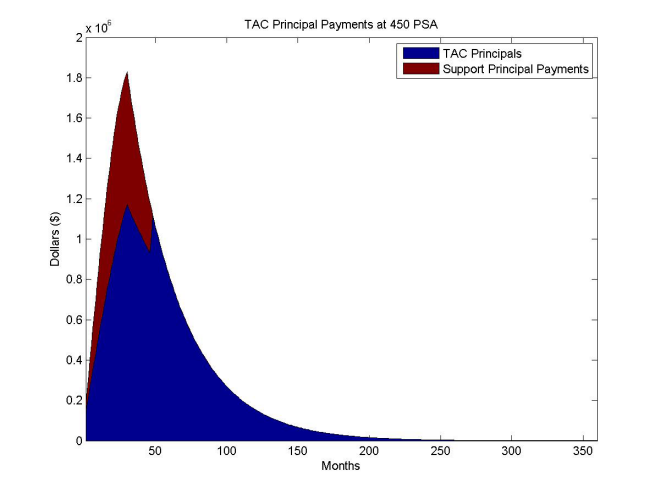

For example, here is a TAC structure rated for 125%, 175%, and 450% PSA.

For prepayments below 175% PSA, the TAC bond extends like a normal sequential pay CMO. TAC bonds are appealing because they offer higher yields than comparable PAC bonds. The unaddressed risk from low prepayment rates generally does not concern investors as much as risk from high prepayment rates.

See Also

cmoseqcf | cmosched | cmoschedcf | mbscfamounts | mbspassthrough