University of Rome Tor Vergata Graduate Students Acquire Marketable Programming and Asset Pricing Skills

“In finance, you only truly understand the theory after you implement it in code and run that code on data to see what it produces—all of which our students do in MATLAB. We know this approach is much appreciated by the industry because our graduates find jobs quite easily.”

Challenge

Teach graduate students in finance and banking the quantitative analysis and coding skills that are in demand in the industry

Solution

Take advantage of campus-wide access to MATLAB, online tutorials, and a certification program to enable students to acquire and demonstrate proficiency in MATLAB programming

Results

- Classroom time optimized

- Complex concepts learned through visualization

- Students graduated with in-demand skills

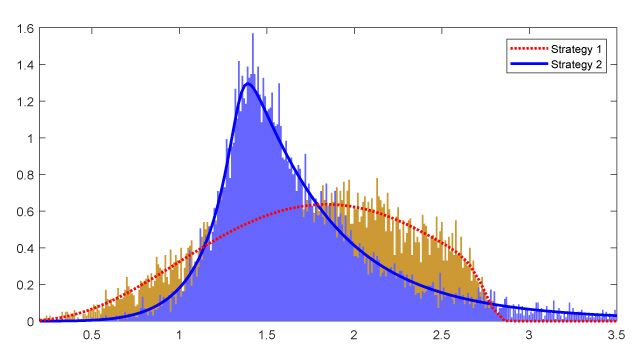

Monte Carlo simulation results for empirical densities returns (bars) and theoretical densities returns (lines) for two dynamic strategies.

The two-year Master of Science in Finance and Banking program at the School of Economics of the University of Rome Tor Vergata is designed for talented students who wish to study the application of mathematical and statistical techniques to financial markets. The program produces graduates with quantitative skills that are in high demand at financial institutions—98% of the students are employed within one year of completing their studies.

Stefano Herzel, professor of mathematics for economics and finance at Tor Vergata, teaches two courses that are very relevant to the master’s program: Coding for Financial Applications and Asset Pricing. By using MATLAB®, Herzel has improved learning outcomes by implementing an intuitive, hands-on approach to lectures and assignments.

“Our students come from different backgrounds, and most have no programming experience when they begin,” says Herzel. “The online resources provided by MathWorks and the user-friendly MATLAB environment make it easy for students to learn quickly. It would be more difficult for them to start with a language like Python or R.”

Challenge

Herzel had several teaching goals for his courses. For Coding for Financial Applications, he wanted to spend more classroom time helping students work through problems and less time on lectures covering the basics. For Asset Pricing, he wanted students to gain a deeper understanding of economic and financial theory by writing code to implement and visualize the concepts they learned.

Among Herzel’s main objectives were to equip students with the quantitative skills sought by prospective employers and provide students with an opportunity to earn a certification to demonstrate their MATLAB proficiency.

Solution

Herzel took advantage of a Campus-Wide License for MATLAB at Tor Vergata to develop content and teach courses for the university’s Master of Science in Finance and Banking program.

Students take Coding for Financial Applications in their first year. They learn how to work with vectors, matrices, and tabular data in MATLAB, as well as how to write functions, handle missing data, and fit models to empirical data.

Before each weekly class session, the students complete tutorials from MATLAB for Financial Applications, an online training course available through the university’s Campus-Wide License. The license enables students to work on their MATLAB assignments on their own laptops anywhere on campus, reducing demand for scarce computer lab time.

Herzel begins each class session by reviewing the material covered in the self-paced online training. He then leads a discussion of the key concepts covered that week. Typically, the students take a quiz and then share their solutions to the quiz problems in MATLAB. Herzel ends the class by introducing the concepts to be covered the following week.

Students in the second-year course Asset Pricing use the MATLAB skills they’ve acquired to complete assignments on various mathematical instruments used in pricing, such as stochastic differential equations, as well as assignments on asset pricing theory, including pricing by arbitrage using the Black-Scholes model or delta hedging.

Assignments include calibrating models via nonlinear least squares optimization, simulating stochastic processes and running Monte Carlo simulations to price derivatives and check the theoretical results of the models.

After completing their coursework, students are given the opportunity to earn the Certified MATLAB Associate credential. Herzel himself was the first professor in Italy to receive MATLAB certification. More than 30 of his students have so far passed the test and become certified.

Tor Vergata faculty are integrating MATLAB into other courses in the Finance and Banking program curriculum, including a course on portfolio management in which students use MATLAB and Optimization Toolbox™ to perform portfolio optimization based on modern portfolio theory.

Results

- Classroom time optimized. “We were already happy with the Campus-Wide License because of the access it provided to MATLAB and the many toolboxes that we use in our program,” says Herzel. “When we discovered that the license also includes a wealth of exceptionally useful online courses, we were even happier, because it meant we could focus classroom time on core material instead of coding basics.”

- Complex concepts learned through visualization. “Stochastic calculus can be confusing, and few students are convinced of its value by a mathematical proof alone,” notes Herzel. “Once they see how it works graphically in MATLAB, however, they are less skeptical, and prepared to apply Black-Scholes and other models that rely on stochastic differential equations.”

- Students graduated with in-demand skills. “One of the strengths of our program is the employment rate of our graduates,” says Herzel. “I often hear from employers how valuable it is for graduates to know how to program, and in our case, to program in MATLAB. MATLAB certification is an additional advantage that dozens of our students achieved last year, and we expect to have as many or more certifications this year.”