ts2func

Convert time series arrays to functions of time and state

Description

Examples

As discussed in Creating SDE Objects, object parameters may be evaluated as if they are MATLAB® functions accessible by a common interface. This accessibility provides the impression of dynamic behavior regardless of whether the underlying parameters are truly time-varying. Furthermore, because parameters are accessible by a common interface, seemingly simple linear constructs may in fact represent complex, nonlinear designs.

For example, consider a univariate geometric Brownian motion (GBM) model of the form:

![]()

In this model, the return, μ(t), and volatility,σ(t), are dynamic parameters of time alone. However, when creating a gbm object to represent the underlying model, such dynamic behavior must be accessible by the common interface. This reflects the fact that GBM models are restricted parameterizations that derive from the general SDE class.

As a convenience, you can specify parameters of restricted models, such as GBM models, as traditional MATLAB® arrays of appropriate dimension. In this case, such arrays represent a static special case of the more general dynamic situation accessible by the interface.

Moreover, when you enter parameters as functions, object constructors can verify that they return arrays of correct size by evaluating them at the initial time and state. Otherwise, object constructors have no knowledge of any particular functional form.

The following example illustrates a technique that includes dynamic behavior by mapping a traditional MATLAB® time series array to a callable function with a interface. It also compares the function with an otherwise identical model with constant parameters.

Because time series arrays represent dynamic behavior that must be captured by functions accessible by the interface, you need utilities to convert traditional time series arrays into callable functions of time and state. The following example shows how to do this using the conversion function ts2func (time series to function).

Load a daily historical data set containing three-month Euribor rates and closing index levels of France's CAC 40 spanning the time interval February 7, 2001 to April 24, 2006.

load Data_GlobalIdx2Simulate risk-neutral sample paths of the CAC 40 index using a geometric Brownian motion (GBM) model:

![]()

where r(t) represents evolution of the risk-free rate of return.

Furthermore, assume that you need to annualize the relevant information derived from the daily data (annualizing the data is optional, but is useful for comparison to other examples), and that each calendar year comprises 250 trading days.

dt = 1/250; returns = tick2ret(Dataset.CAC); sigma = std(returns)*sqrt(250); yields = Dataset.EB3M; yields = 360*log(1 + yields);

Compare the resulting sample paths obtained from two risk-neutral historical simulation approaches, where the daily Euribor yields serve as a proxy for the risk-free rate of return.

The first approach specifies the risk-neutral return as the sample average of Euribor yields, and therefore assumes a constant (non-dynamic) risk-free return.

nPeriods = length(yields); % Simulated observations rng(5713,'twister') obj = gbm(mean(yields),diag(sigma),'StartState',100)

obj =

Class GBM: Generalized Geometric Brownian Motion

------------------------------------------------

Dimensions: State = 1, Brownian = 1

------------------------------------------------

StartTime: 0

StartState: 100

Correlation: 1

Drift: drift rate function F(t,X(t))

Diffusion: diffusion rate function G(t,X(t))

Simulation: simulation method/function simByEuler

Return: 0.0278117

Sigma: 0.231906

[X1,T] = simulate(obj,nPeriods,'DeltaTime',dt);In contrast, the second approach specifies the risk-neutral return as the historical time series of Euribor yields. It therefore assumes a dynamic, yet deterministic, rate of return; this example does not illustrate stochastic interest rates. To illustrate this dynamic effect, use the ts2func utility.

r = ts2func(yields,'Times',(0:nPeriods - 1)');ts2func packages a specified time series array inside a callable function of time and state, and synchronizes it with an optional time vector. For instance:

r(0,100)

ans = 0.0470

evaluates the function at (t = 0, = 100) and returns the first observed Euribor yield.

However, you can also evaluate the resulting function at any intermediate time t and state :

r(7.5,200)

ans = 0.0472

Furthermore, the following command produces the same result when called with time alone:

r(7.5)

ans = 0.0472

The equivalence of these last two commands highlights some important features.

When you specify parameters as functions, they must evaluate properly when passed a scalar, real-valued sample time (t), and an NVars-by-1 state vector (). They must also generate an array of appropriate dimensions, which in the first case is a scalar constant, and in the second case is a scalar, piecewise constant function of time alone. You are not required to use either time (t) or state (). In the current example, the function evaluates properly when passed time followed by state, thereby satisfying the minimal requirements. The fact that it also evaluates correctly when passed only time simply indicates that the function does not require the state vector . The important point to make is that it works when you pass it .

Furthermore, the ts2func function performs a zero-order-hold (ZOH) piecewise constant interpolation. The notion of piecewise constant parameters is pervasive throughout the SDE architecture, and is discussed in more detail in Optimizing Accuracy: About Solution Precision and Error.

Complete the comparison by performing the second simulation using the same initial random number state. Simulate paths using a dynamic, deterministic rate of return.

rng(5713,'twister') obj = gbm(r, diag(sigma),'StartState',100)

obj =

Class GBM: Generalized Geometric Brownian Motion

------------------------------------------------

Dimensions: State = 1, Brownian = 1

------------------------------------------------

StartTime: 0

StartState: 100

Correlation: 1

Drift: drift rate function F(t,X(t))

Diffusion: diffusion rate function G(t,X(t))

Simulation: simulation method/function simByEuler

Return: function ts2func/vector2Function

Sigma: 0.231906

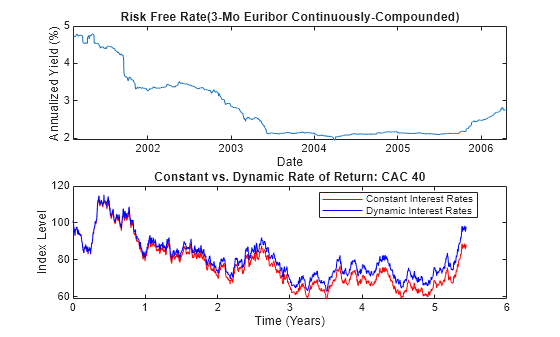

X2 = simulate(obj,nPeriods,'DeltaTime',dt);Plot the series of risk-free reference rates to compare the two simulation trials.

subplot(2,1,1) dates = datetime(dates,"ConvertFrom","datenum"); plot(dates,100*yields) xlabel('Date') ylabel('Annualized Yield (%)') title('Risk Free Rate(3-Mo Euribor Continuously-Compounded)') subplot(2,1,2) plot(T,X1,'red',T,X2,'blue') xlabel('Time (Years)') ylabel('Index Level') title('Constant vs. Dynamic Rate of Return: CAC 40') legend({'Constant Interest Rates' 'Dynamic Interest Rates'},... 'Location', 'Best')

The paths are close but not exact. The blue line in the last plot uses all the historical Euribor data, and illustrates a single trial of a historical simulation.

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

When you specify

Arrayas a scalar or a vector (row or column),ts2funcassumes that it represents a univariate time series.Freturns an array with one less dimension than the input time series arrayArraywith whichFis associated. Thus, whenArrayis a vector, a 2-dimensional matrix, or a three-dimensional array,Freturns a scalar, vector, or 2-dimensional matrix, respectively.When the scalar time t at which

ts2funcevaluates the functionFdoes not coincide with an observation time inTimes,Fperforms a zero-order-hold interpolation. The only exception is if t precedes the first element ofTimes, in which case F(t) = F(Times(1)).To support Monte Carlo simulation methods, the output function

Freturns anNVars-by-1column vector or a two-dimensional matrix withNVarsrows.The output function

Fis always a deterministic function of time, F(t), and may always be called with a single input regardless of theDeterministicflag. The distinction is that whenDeterministicis false, the functionFmay also be called with a second input, anNVars-by-1state vector X(t), which is a placeholder and ignored. While F(t) and F(t,X) produce identical results, the former specifically indicates that the function is a deterministic function of time, and may offer significant performance benefits in some situations.

References

[1] Aït-Sahalia, Y. “Testing Continuous-Time Models of the Spot Interest Rate.” The Review of Financial Studies, Spring 1996, Vol. 9, No. 2, pp. 385–426.

[2] Aït-Sahalia, Y. “Transition Densities for Interest Rate and Other Nonlinear Diffusions.” The Journal of Finance, Vol. 54, No. 4, August 1999.

[3] Glasserman, P. Monte Carlo Methods in Financial Engineering. New York, Springer-Verlag, 2004.

[4] Hull, J. C. Options, Futures, and Other Derivatives, 5th ed. Englewood Cliffs, NJ: Prentice Hall, 2002.

[5] Johnson, N. L., S. Kotz, and N. Balakrishnan. Continuous Univariate Distributions. Vol. 2, 2nd ed. New York, John Wiley & Sons, 1995.

[6] Shreve, S. E. Stochastic Calculus for Finance II: Continuous-Time Models. New York: Springer-Verlag, 2004.

Version History

Introduced in R2008a