Statistics

53 Posts

RANK

N/A

of 302,006

REPUTATION

N/A

CONTRIBUTIONS

0 Questions

0 Answers

ANSWER ACCEPTANCE

0.00%

VOTES RECEIVED

0

RANK

of 21,488

REPUTATION

N/A

AVERAGE RATING

0.00

CONTRIBUTIONS

0 Files

DOWNLOADS

0

ALL TIME DOWNLOADS

0

RANK

of 178,011

CONTRIBUTIONS

0 Problems

0 Solutions

SCORE

0

NUMBER OF BADGES

0

CONTRIBUTIONS

53 Posts

CONTRIBUTIONS

0 Public Channels

AVERAGE RATING

CONTRIBUTIONS

0 Discussions

AVERAGE NO. OF LIKES

Feeds

Published

Responding to SR 26-2: From Strategic Interpretation to Practical Evidence | Part 2 of 4

Where SR 26-2 Creates Flexibility—and Where It Does Not The opportunity is real, but it is narrower, more conditional, and...

2 days ago

Published

Responding to SR 26-2: From Strategic Interpretation to Practical Evidence | Part 1 of 4

SR 26-2 Did Not Lighten the Load. It Moved the Burden of Proof. The real change is not the shorter guidance. It is the...

9 days ago

Published

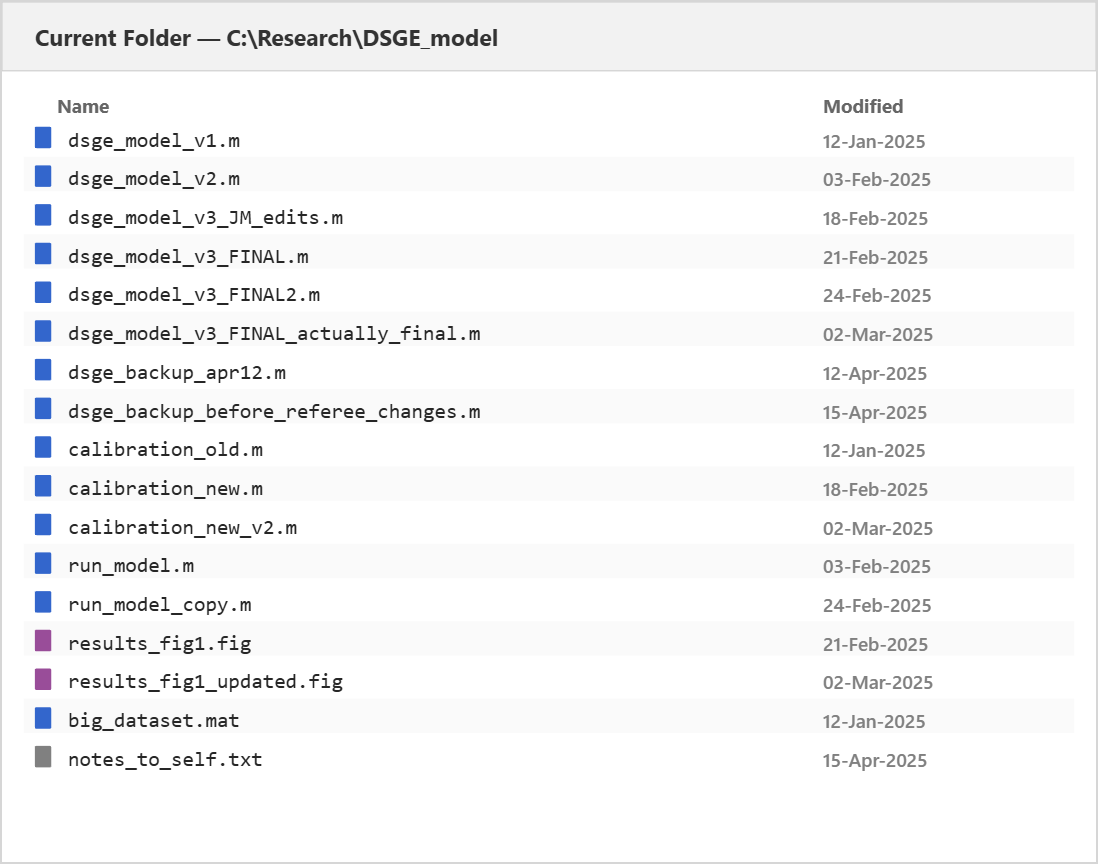

Version Control for Economic Models

A Practical Guide to Git in MATLAB The Problem You Already Have You know the folder. Somewhere on your machine there...

1 month ago

Published

From EViews to MATLAB in One Line: Reading Workfiles Directly

Economists often keep years of work in EViews workfiles: macroeconomic series, model estimates, and curated panel data. The...

2 months ago

Published

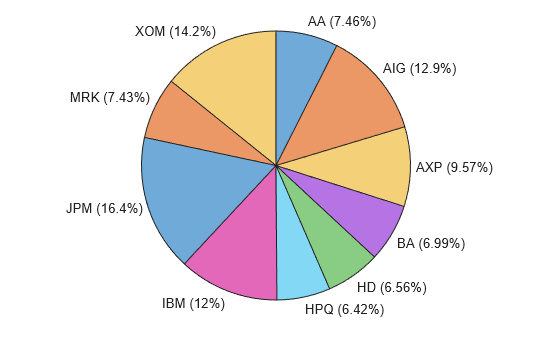

Portfolio Optimization with Target Factor Exposures

A practical MATLAB walkthrough comparing tracking error and exact exposure approaches. When you build a factor-based...

3 months ago

Published

Prototype Time-Series Forecasts with Deep Learning—Without Writing Code

Expert Contributor: Dr. Yuchen Dong Yuchen is a Senior Application Engineer at MathWorks focusing on customers in the...

3 months ago

Published

Run Dynare at Scale on Databricks with Interactive MATLAB

Expert Contributor: Dr. Eduard Benet Cerdà Edu is a Senior Application Engineer at MathWorks advising customers in the...

4 months ago

Published

What’s New in MATLAB R2026a for Economists

R2026a covers a lot of ground for economists—Bayesian state-space estimation, macro-scale forecasting, climate and physical...

4 months ago

Published

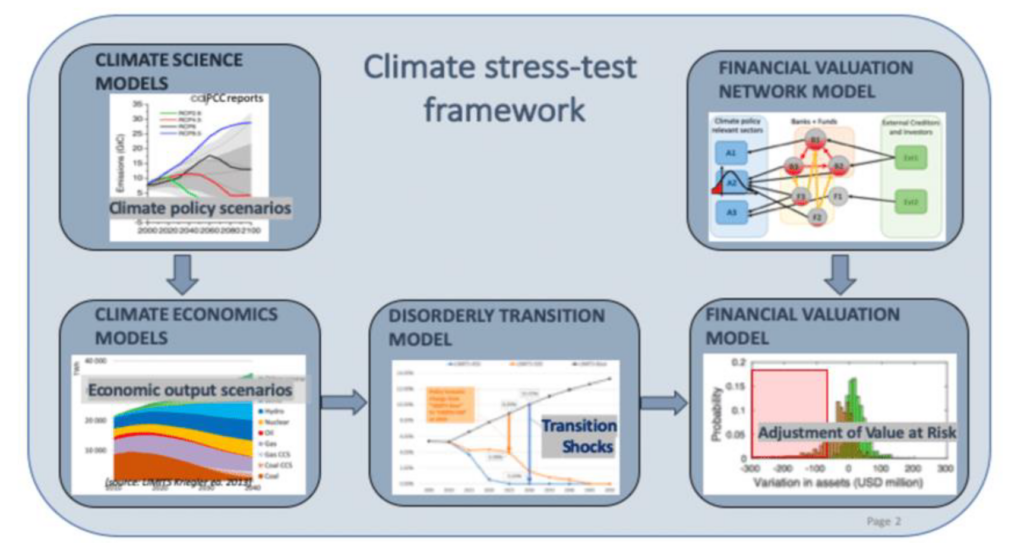

CRISK: A Market‑Based Framework for Quantifying Climate Risk in Banking

Effective risk management increasingly requires understanding how climate‑related factors can influence market valuations...

5 months ago

Published

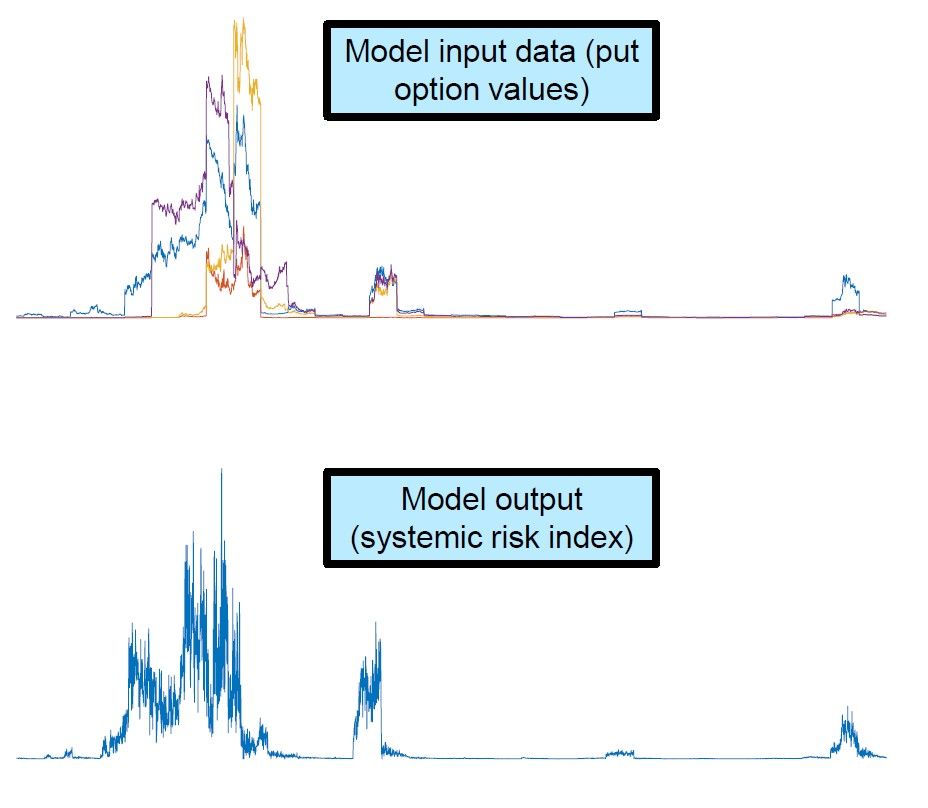

Systemic Risk Modeling with MATLAB: Tools and Techniques for Central Banks

Systemic risk modeling is essential for central banks as financial systems grow more interconnected and vulnerable to...

5 months ago

Published

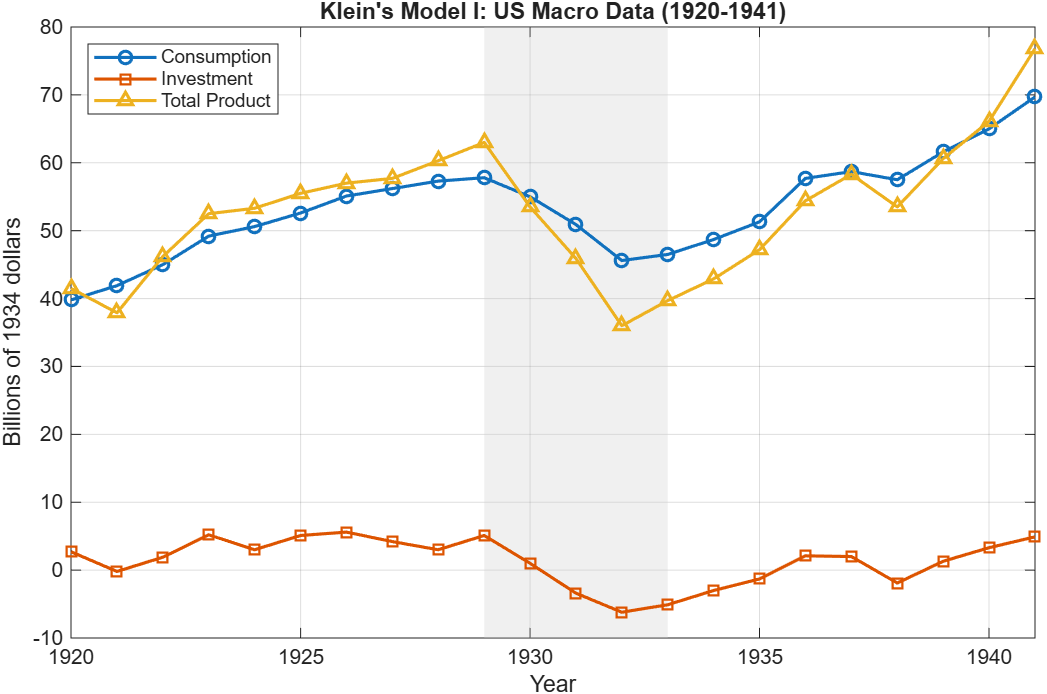

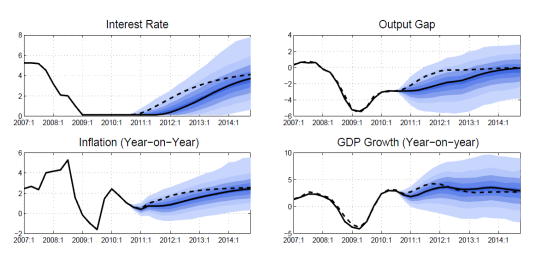

Refining Macroeconomic Forecasting with MATLAB Techniques

Nonlinear confidence bands help you quantify forecast uncertainty in DSGE models, but they can be slow to compute. At the...

5 months ago

Published

Upgrading MATLAB: What You Gain and How to Get There

Every MATLAB release opens the door to new capabilities, better performance, and tighter integration with the platforms...

5 months ago

Published

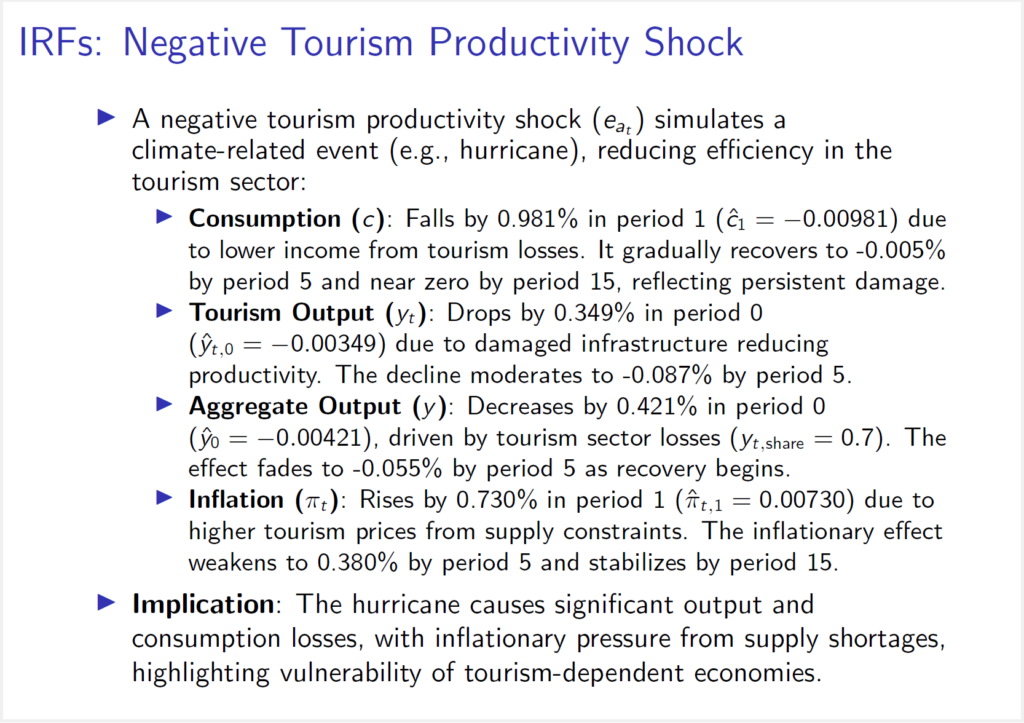

Central Bank of The Bahamas Uses MATLAB and Dynare to Model Climate and Tourism Shocks

“It [MATLAB] was used in Dynare in order to promote the accuracy and the ease of generating this model.”— Allan Wright,...

6 months ago

Published

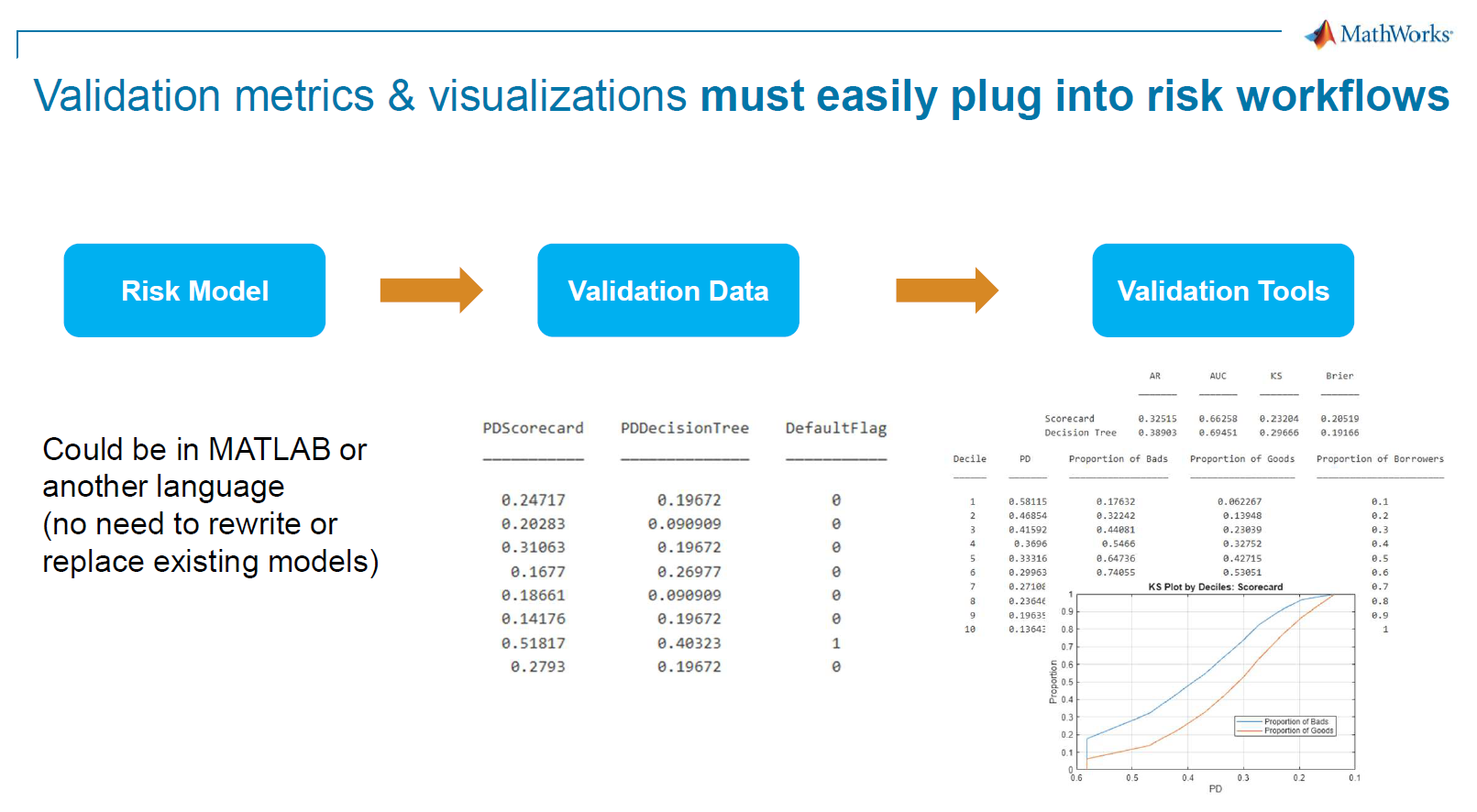

Credit and Market Risk Management: From Risk Modeling to Regulatory Compliance

In this technical session, Valerio Sperandeo, Senior Application Engineer, demonstrated how MATLAB can support financial...

8 months ago

Published

Speeding Up Dynare Models: Practical Paths to Performance Gains

Dynamic Stochastic General Equilibrium (DSGE) models are essential tools for policy analysis and forecasting, but...

8 months ago

Published

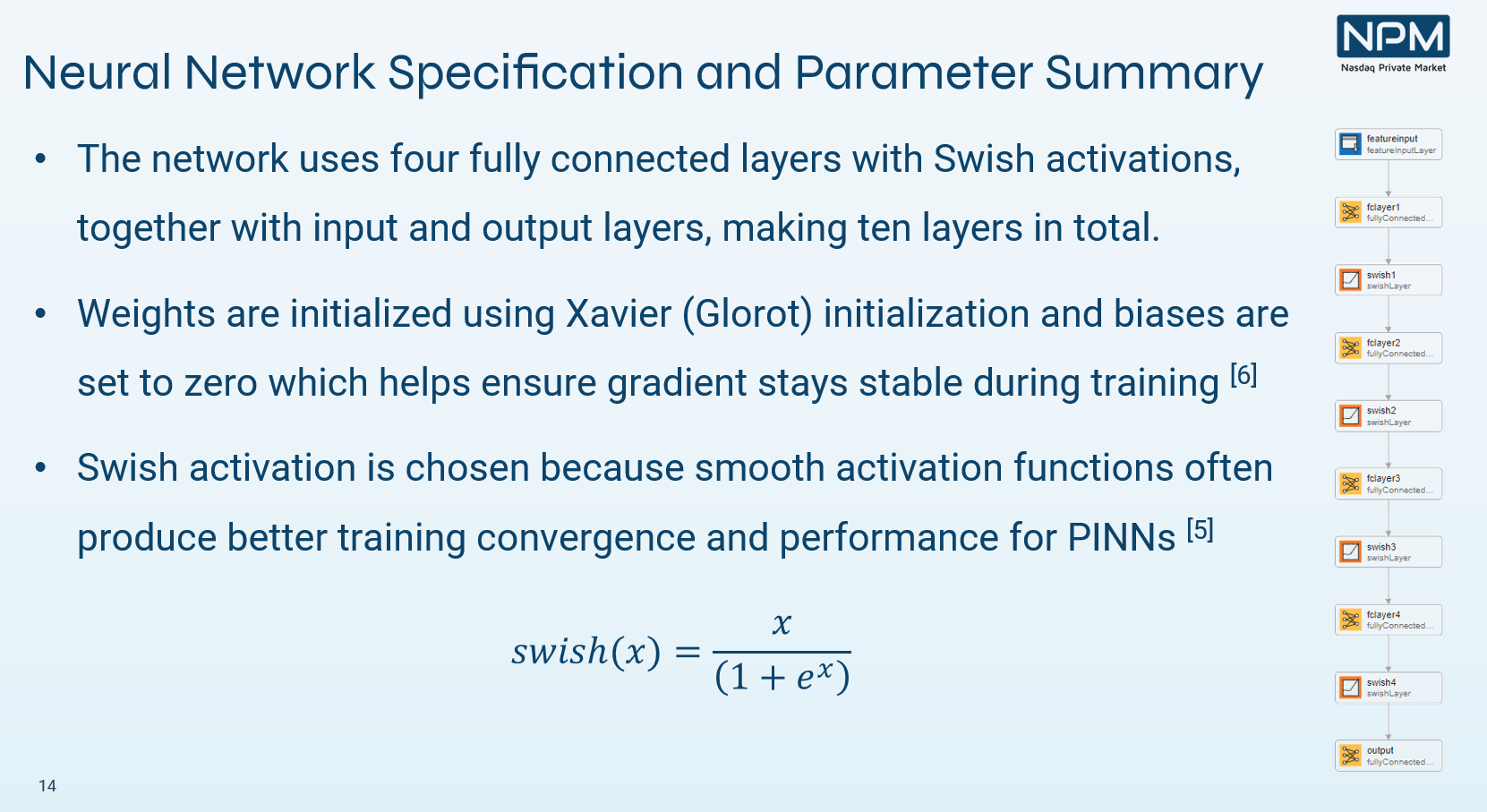

Pricing Special Purpose Vehicles with Physics‑Informed Neural Networks at Nasdaq Private Market

Summary Nasdaq Private Market (NPM) used MATLAB® to prototype and scale physics‑informed neural networks (PINNs) that price...

9 months ago

Published

Highlights from MathWorks Finance Conference 2025

The 2025 MathWorks Finance Conference brought together quants, economists, financial modelers and researchers to explore...

9 months ago

Published

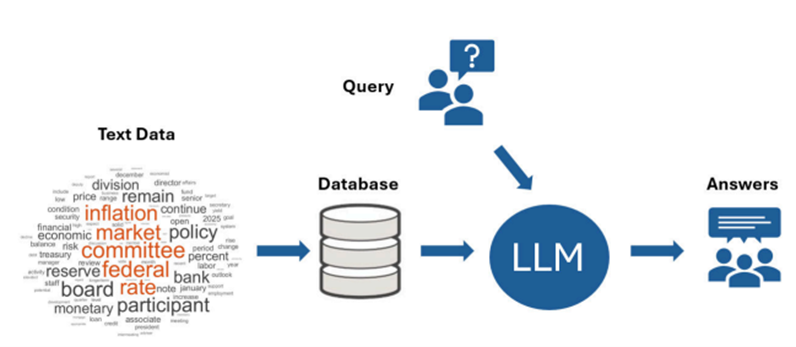

Build a RAG Pipeline in MATLAB: From Document Ingestion to LLM-Driven Insights

The following post is from Yuchen Dong, Senior Finance Application Engineer at MathWorks. The example featured in the...

10 months ago

Published

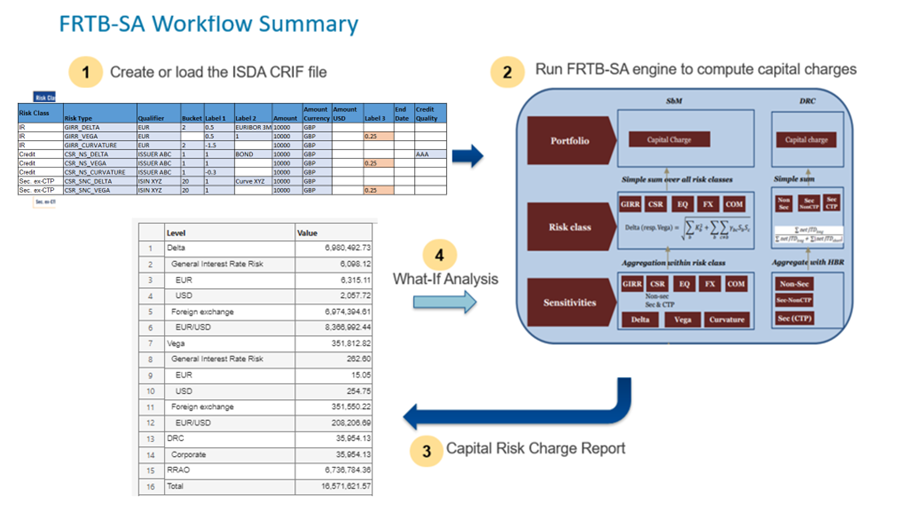

Navigating FRTB: Standardized vs Internal Models – and the Role of Scriptable Risk Engines

The Fundamental Review of the Trading Book (FRTB) is reshaping how banks measure and manage market risk. Beyond replacing...

10 months ago

Published

The FRED Connector in Datafeed Toolbox

If you work with macro, markets, or policy analysis, chances are you touch FRED®—the Federal Reserve Economic Data service....

11 months ago

Published

Analyzing the Financial Risks of Wildfires

We recently hosted a technical webinar focused on analyzing the financial risks of wildfires. Akshay Paul and Yuchen Dong...

11 months ago

Published

Building a Neural Network for Time Series Forecasting – Low-Code Workflow

The following post is from Yuchen Dong, Senior Financial Application Engineer at MathWorks. Financial institutions forecast...

1 year ago

Published

GDP Nowcasting with MATLAB

What is GDP Nowcasting? Imagine trying to drive a car while only getting speed updates every three months. That’s kind of...

1 year ago

Published

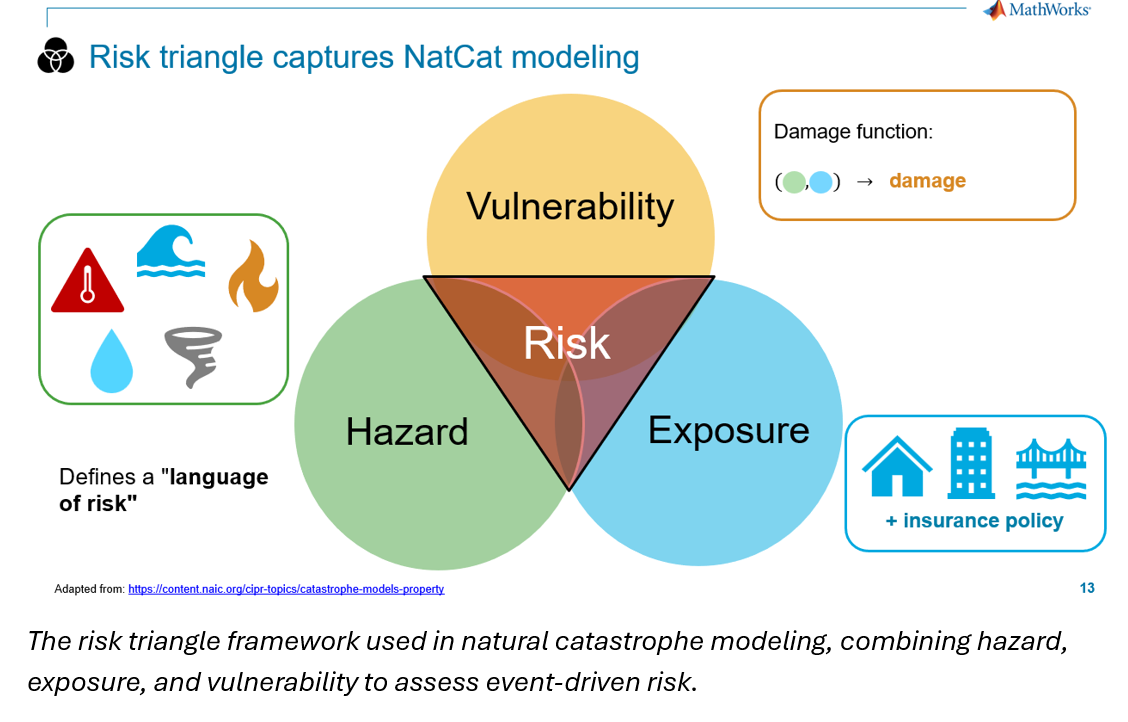

Modeling Physical Climate Risk Across Financial Portfolios

Financial institutions are reassessing long-term risk models as physical climate events like hurricanes, floods, and...

1 year ago

Published

Accelerating Asset Management with ModelOps: From Model Building to Monitoring

Asset management quants face complex data environments, tight timelines, and the constant pressure to translate models into...

1 year ago

Published

2nd Biennial Macroeconometric Caribbean Conference

MathWorks was recently invited to the 2nd Biennial Macroeconometric Caribbean Conference in Nassau, Bahamas, organized by...

1 year ago

Published

The Economic Effects of Tariff Changes

The following post is from Yuchen Dong, Senior Financial Application Engineer. The code presented in this blog can be found...

1 year ago

Published

Modeling Exchange Rate Volatility

The following post is from William Mueller, Software Developer on the Econometrics Toolbox Team. Forecasting currency...

1 year ago

Published

Assessing Climate Impacts on Credit Risk

We recently hosted a technical webinar focused on climate transition risk, specifically assessing climate impacts on credit...

1 year ago

Published

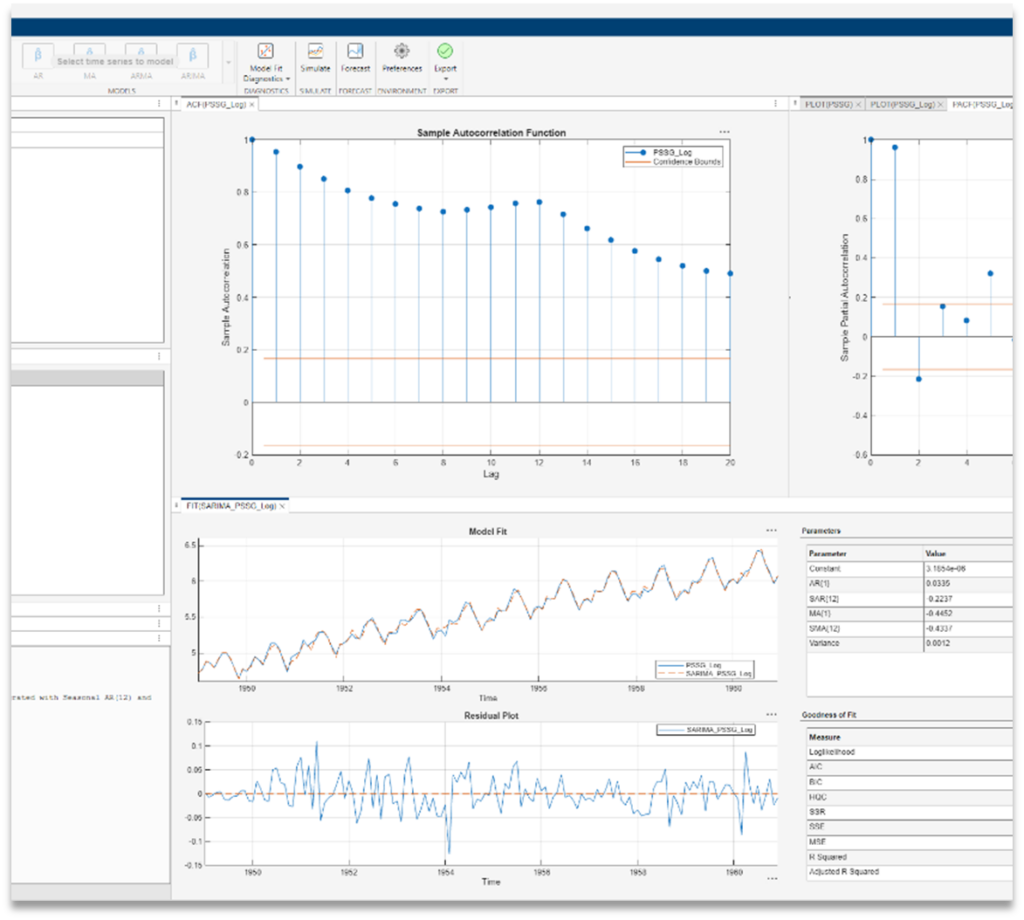

Simplifying Econometric Modeling with MATLAB

Econometric modeling is essential for analyzing economic data, making forecasts, and informing policy decisions, however,...

1 year ago