Calibrating Hull-White Model Using Market Data

The pricing of interest-rate derivative securities relies on models that describe the underlying process. These interest rate models depend on one or more parameters that you must determine by matching the model predictions to the existing data available in the market. In the Hull-White model, there are two parameters related to the short rate process: mean reversion and volatility. Calibration is used to determine these parameters, such that the model can reproduce, as close as possible, the prices of caps or floors observed in the market. The calibration routines find the parameters that minimize the difference between the model price predictions and the market prices for caps and floors.

For a Hull-White model, the minimization is two dimensional, with respect to mean reversion (α) and volatility (σ). That is, calibrating the Hull-White model minimizes the difference between the model’s predicted prices and the observed market prices of the corresponding caplets or floorlets.

Hull-White Model Calibration Example

Use market data to identify the implied volatility (σ) and mean reversion (α)

coefficients needed to build a Hull-White tree to price an instrument. The ideal

case is to use the volatilities of the caps or floors used to calculate

Alpha (α) and Sigma (σ). This will most

likely not be the case, so market data must be interpolated to obtain the required

values.

Consider a cap with these parameters:

Settle = 'Jan-21-2008'; Maturity = 'Mar-21-2011'; Strike = 0.0690; Reset = 4; Principal = 1000; Basis = 0;

The caplets for this example would fall in:

capletDates = cfdates(Settle, Maturity, Reset, Basis); datestr(capletDates')

ans = 21-Mar-2008 21-Jun-2008 21-Sep-2008 21-Dec-2008 21-Mar-2009 21-Jun-2009 21-Sep-2009 21-Dec-2009 21-Mar-2010 21-Jun-2010 21-Sep-2010 21-Dec-2010 21-Mar-2011

In the best case, look up the market volatilities for caplets with a

Strike = 0.0690, and maturities in each

reset date listed, but the likelihood of finding these exact instruments is low. As

a consequence, use data that is available in the market and interpolate to find

appropriate values for the caplets.

Based on the market data, you have the cap information for different dates and

strikes. Assume that instead of having the data for Strike =

0.0690, you have the data for Strike1 =

0.0590 and Strike2 =

0.0790.

| Maturity | Strike1 = 0.0590 | Strike2 = 0.0790 |

|---|---|---|

| 21-Mar-2008 | 0.1533 | 0. 1526 |

| 21-Jun-2008 | 0.1731 | 0. 1730 |

| 21-Sep-2008 | 0. 1727 | 0. 1726 |

| 21-Dec-2008 | 0. 1752 | 0. 1747 |

| 21-Mar-2009 | 0. 1809 | 0. 1808 |

| 21-Jun-2009 | 0. 1809 | 0. 1792 |

| 21-Sep-2009 | 0. 1805 | 0. 1797 |

| 21-Dec-2009 | 0. 1802 | 0. 1794 |

| 21-Mar-2010 | 0. 1802 | 0. 1733 |

| 21-Jun-2010 | 0. 1757 | 0. 1751 |

| 21-Sep-2010 | 0. 1755 | 0. 1750 |

| 21-Dec-2010 | 0. 1755 | 0. 1745 |

| 21-Mar-2011 | 0. 1726 | 0. 1719 |

The nature of this data lends itself to matrix nomenclature, which is perfect for

MATLAB®. hwcalbycap requires that the

dates, the strikes, and the actual volatility be separated into three variables:

MarketStrike, MarketMat, and

MarketVol.

MarketStrike = [0.0590; 0.0790]; MarketMat = [datetime(2008,3,21) ; datetime(2008,6,21) ; datetime(2008,9,21) ; datetime(2008,12,21) ; datetime(2009,3,21) ; ... datetime(2009,6,21) ; datetime(2009,9,21) ; datetime(2009,12,21); datetime(2010,3,21) ; ... datetime(2010,6,21); datetime(2010,9,21) ; datetime(2010,12,21) ; datetime(2011,3,21)]; MarketVol = [0.1533 0.1731 0.1727 0.1752 0.1809 0.1800 0.1805 0.1802 0.1735 0.1757 ... 0.1755 0.1755 0.1726; % First row in table corresponding to Strike1 0.1526 0.1730 0.1726 0.1747 0.1808 0.1792 0.1797 0.1794 0.1733 0.1751 ... 0.1750 0.1745 0.1719]; % Second row in table corresponding to Strike2

Complete the input arguments using this data for

RateSpec:

Rates = [0.0627; 0.0657; 0.0691; 0.0717; 0.0739; 0.0755; 0.0765; 0.0772; 0.0779; 0.0783; 0.0786; 0.0789; 0.0792; 0.0793]; ValuationDate = datetime(2008,1,21); EndDates = [datetime(2008,3,21) ; datetime(2008,6,21) ; datetime(2008,9,21) ; datetime(2008,12,21) ; ... datetime(2009,3,21) ; datetime(2009,6,21) ; datetime(2009,9,21) ; datetime(2009,12,21); datetime(2010,3,21) ; ... datetime(2010,6,21); datetime(2010,9,21) ; datetime(2010,12,21) ; datetime(2011,3,21) ; datetime(2011,6,21)]; Compounding = 4; Basis = 0; RateSpec = intenvset('ValuationDate', ValuationDate, ... 'StartDates', ValuationDate, 'EndDates', EndDates, ... 'Rates', Rates, 'Compounding', Compounding, 'Basis', Basis)

RateSpec =

FinObj: 'RateSpec'

Compounding: 4

Disc: [14x1 double]

Rates: [14x1 double]

EndTimes: [14x1 double]

StartTimes: [14x1 double]

EndDates: [14x1 double]

StartDates: 733428

ValuationDate: 733428

Basis: 0

EndMonthRule: 1Call the calibration routine to find values for volatility parameters Alpha and Sigma

Use hwcalbycap to calculate the

values of Alpha and Sigma based on market

data. Internally, hwcalbycap calls the function

lsqnonlin. You can customize

lsqnonlin by passing an

optimization options structure created by optimoptions and then this can be

passed to hwcalbycap using the

name-value pair argument for OptimOptions. For example,

optimoptions defines the target

objective function tolerance as 100*eps and then calls

hwcalbycap:

o=optimoptions('lsqnonlin','TolFun',100*eps); [Alpha, Sigma] = hwcalbycap(RateSpec, MarketStrike, MarketMat, MarketVol, ... Strike, Settle, Maturity, 'Reset', Reset, 'Principal', Principal, 'Basis', ... Basis, 'OptimOptions', o)

Local minimum possible.

lsqnonlin stopped because the size of the current step is less than

the default value of the step size tolerance.

Warning: LSQNONLIN did not converge to an optimal solution. It exited with exitflag = 2.

> In hwcalbycapfloor at 93

In hwcalbycap at 75

Alpha =

1.0000e-06

Sigma =

0.0127 The previous warning indicates that the conversion was not optimal. The

search algorithm used by the Optimization Toolbox™ function lsqnonlin did not find a solution

that conforms to all the constraints. To discern whether the solution is

acceptable, look at the results of the optimization by specifying a third output

(OptimOut) for hwcalbycap:

[Alpha, Sigma, OptimOut] = hwcalbycap(RateSpec, MarketStrike, MarketMat, ... MarketVol, Strike, Settle, Maturity, 'Reset', Reset, 'Principal', Principal, ... 'Basis', Basis, 'OptimOptions', o);

The OptimOut.residual field of the

OptimOut structure is the optimization residual. This

value contains the difference between the Black caplets and those calculated

during the optimization. You can use the OptimOut.residual

value to calculate the percentual difference (error) compared to Black caplet

prices and then decide whether the residual is acceptable. There is almost

always some residual, so decide if it is acceptable to parameterize the market

with a single value of Alpha and

Sigma.

Price caplets using market data and Black's formula to obtain reference caplet values

To determine the effectiveness of the optimization, calculate reference caplet values using Black’s formula and the market data. Note, you must first interpolate the market data to obtain the caplets for calculation:

[Mats, Strikes] = meshgrid(MarketMat, MarketStrike);

MarketMat_T = yearfrac(Settle,Mats);

Mats_T = yearfrac(Settle,Maturity);

FlatVol = interp2(MarketMat_T, Strikes, MarketVol, Mats_T, Strike, 'spline');

Compute the price of the cap using the Black model:

[CapPrice, Caplets] = capbyblk(RateSpec, Strike, Settle, Maturity, FlatVol, ... 'Reset', Reset, 'Basis', Basis, 'Principal', Principal); Caplets = Caplets(2:end)';

Caplets =

0.3210

1.6355

2.4863

3.1903

3.4110

3.2685

3.2385

3.4803

3.2419

3.1949

3.2991

3.3750Compare optimized values and Black values and display graphically

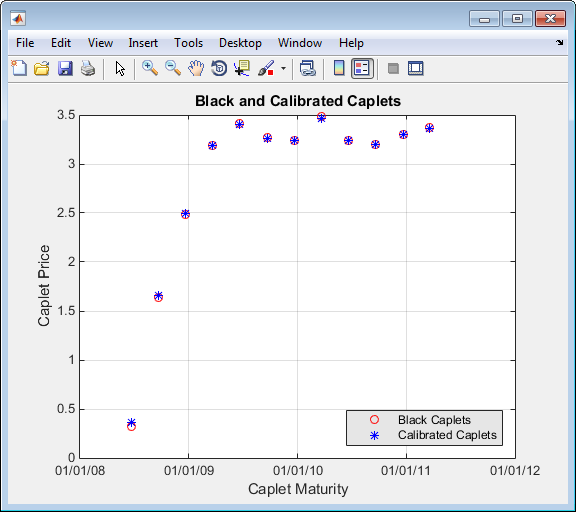

After calculating the reference values for the caplets, compare the values,

analytically and graphically, to determine whether the calculated single values

of Alpha and Sigma provide an adequate

approximation:

OptimCaplets = Caplets+OptimOut.residual; disp(' '); disp(' Black76 Calibrated Caplets'); disp([Caplets OptimCaplets]) plot(MarketMat(2:end), Caplets, 'or', MarketMat(2:end), OptimCaplets, '*b'); xtickformat; xlabel('Caplet Maturity'); ylabel('Caplet Price'); title('Black and Calibrated Caplets'); h = legend('Black Caplets', 'Calibrated Caplets'); set(h, 'color', [0.9 0.9 0.9]); set(h, 'Location', 'SouthEast'); set(gcf, 'NumberTitle', 'off') grid on

Black76 Calibrated Caplets

0.3210 0.3636

1.6355 1.6603

2.4863 2.4974

3.1903 3.1874

3.4110 3.4040

3.2685 3.2639

3.2385 3.2364

3.4803 3.4683

3.2419 3.2408

3.1949 3.1957

3.2991 3.2960

3.3750 3.3663

Compare cap prices using the Black, HW analytical, and HW tree models

Using the calculated caplet values, compare the prices of the corresponding

cap using the Black model, Hull-White analytical, and Hull-White tree models. To

calculate a Hull-White tree based on Alpha and

Sigma, use these calibration routines:

Black model:

CapPriceBLK = CapPrice;

HW analytical model:

CapPriceHWAnalytical = sum(OptimCaplets);

HW tree model to price the cap derived from the calibration process:

Create

VolSpecfrom the calibration parametersAlphaandSigma:VolDates = EndDates; VolCurve = Sigma*ones(14,1); AlphaDates = EndDates; AlphaCurve = Alpha*ones(14,1); HWVolSpec = hwvolspec(ValuationDate, VolDates, VolCurve,AlphaDates, AlphaCurve);

Create the

TimeSpec:HWTimeSpec = hwtimespec(ValuationDate, EndDates, Compounding);

Build the HW tree using the

HW2000method:HWTree = hwtree(HWVolSpec, RateSpec, HWTimeSpec, 'Method', 'HW2000');

Price the cap:

Price = capbyhw(HWTree, Strike, Settle, Maturity, Reset, Basis, Principal); disp(' '); disp([' CapPrice Black76 ..................: ', num2str(CapPriceBLK,'%15.5f')]); disp([' CapPrice HW analytical..........: ', num2str(CapPriceHWAnalytical,'%15.5f')]); disp([' CapPrice HW from capbyhw ..: ', num2str(Price,'%15.5f')]); disp(' ');

CapPrice Black76 ..........: 34.14220 CapPrice HW analytical.....: 34.18008 CapPrice HW from capbyhw ..: 34.14192

Price a portfolio of instruments using the calibrated HW tree

After building a Hull-White tree, based on parameters calibrated from market

data, use HWTree to price a portfolio of these instruments:

Two bonds

CouponRate = [0.07; 0.09]; Settle = 'Jan-21-2008'; Maturity = {'Mar-21-2010';'Mar-21-2011'}; Period = 1; Face = 1000; Basis = 0;

Bond with an embedded American call option

CouponRateOEB = 0.08; SettleOEB = 'Jan-21-2008'; MaturityOEB = 'Mar-21-2011'; OptSpec = 'call'; StrikeOEB = 950; ExerciseDatesOEB = 'Mar-21-2011'; AmericanOpt = 1; Period = 1; Face = 1000; Basis = 0;

To price this portfolio of instruments using the calibrated

HWTree:

Use

instaddto create the portfolioInstSet:InstSet = instadd('Bond', CouponRate, Settle, Maturity, Period, Basis, [], [], [], [], [], Face); InstSet = instadd(InstSet,'OptEmBond', CouponRateOEB, SettleOEB, MaturityOEB, OptSpec, ... StrikeOEB, ExerciseDatesOEB, 'AmericanOpt', AmericanOpt, 'Period', Period, ... 'Face',Face, 'Basis', Basis);

Add the cap instrument used in the calibration:

SettleCap = ' Jan-21-2008'; MaturityCap = 'Mar-21-2011'; StrikeCap = 0.0690; Reset = 4; Principal = 1000; InstSet = instadd(InstSet,'Cap', StrikeCap, SettleCap, MaturityCap, Reset, Basis, Principal);

Assign names to the portfolio instruments:

Names = {'7% Bond'; '8% Bond'; 'BondEmbCall'; '6.9% Cap'}; InstSet = instsetfield(InstSet, 'Index',1:4, 'FieldName', {'Name'}, 'Data', Names );Examine the set of instruments contained in

InstSet:instdisp(InstSet)

IdxType CoupRate Settle Mature Period Basis EOMRule IssueDate 1stCoupDate LastCoupDate StartDate Face Name 1 Bond 0.07 21-Jan-2008 21-Mar-2010 1 0 NaN NaN NaN NaN NaN 1000 7% Bond 2 Bond 0.09 21-Jan-2008 21-Mar-2011 1 0 NaN NaN NaN NaN NaN 1000 8% Bond IdxType CoupRate Settle Mature OptSpec Stke ExDate Per Basis EOMRule IssDate 1stCoupDate LstCoupDate StrtDate Face AmerOpt Name 3 OptEmBond 0.08 21-Jan-2008 21-Mar-2011 call 950 21-Jan-2008 21-Mar-2011 1 0 1 NaN NaN NaN NaN 1000 1 BondEmbCall Index Type Strike Settle Maturity CapReset Basis Principal Name 4 Cap 0.069 21-Jan-2008 21-Mar-2011 4 0 1000 6.9% Cap

Use

hwpriceto price the portfolio using the calibratedHWTree:format bank PricePortfolio = hwprice(HWTree, InstSet)PricePortfolio = 980.45 1023.05 945.73 34.14

See Also

instbond | instcap | instoptbnd | instoptembnd | intenvset | hwtimespec | hwtree | hwvolspec | bondbyhw | capbyhw | hwcalbycap | hwcalbyfloor | hwprice | hwsens

Topics

- Overview of Interest-Rate Tree Models

- Pricing Using Interest-Rate Tree Models

- Graphical Representation of Trees

- Understanding Interest-Rate Tree Models

- Understanding Interest-Rate Term Structure

- Pricing Using Interest-Rate Term Structure

- Supported Interest-Rate Instrument Functions

- Supported Equity Derivative Functions

- Supported Energy Derivative Functions

- Mapping Financial Instruments Toolbox Functions for Interest-Rate Instrument Objects