backtestEngine

Create backtestEngine object to backtest strategies and

analyze results

Description

Create a backtestEngine to run a backtest of portfolio

investment strategies on historical data.

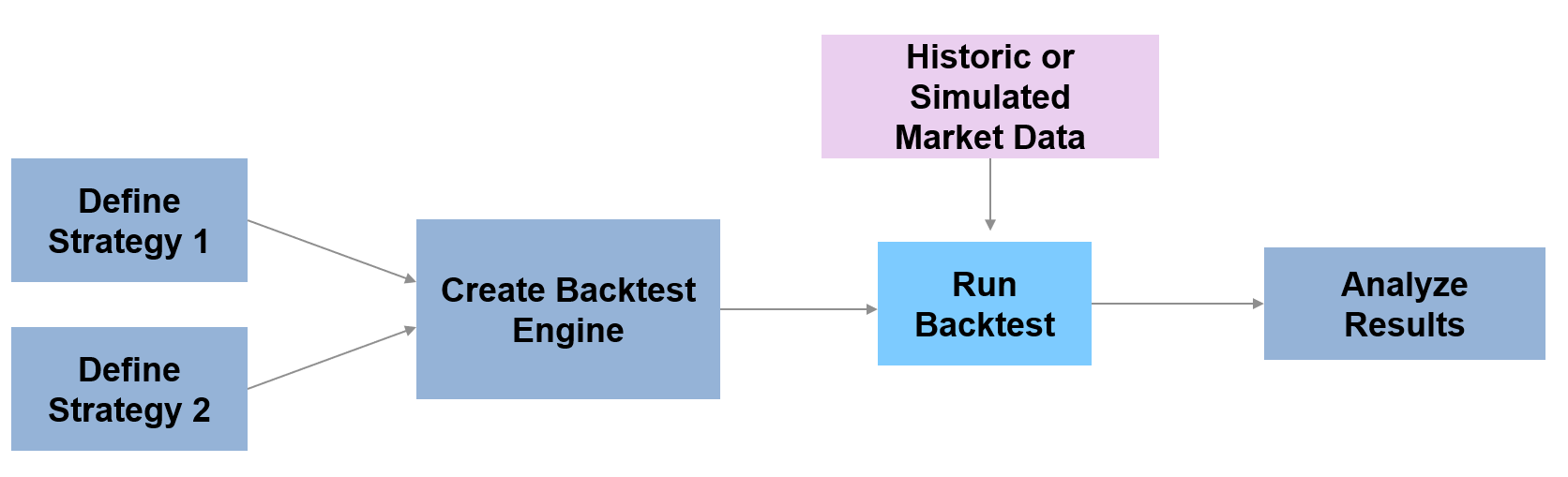

Use this workflow to develop and run a backtest:

Define the strategy logic using a

backtestStrategyobject to specify how a strategy rebalances a portfolio of assets.Use

backtestEngineto create abacktestEngineobject that specifies parameters of the backtest.Use

runBacktestto run the backtest against historical asset price data and, optionally, trading signal data.Use

equityCurveto plot the equity curves of each strategy.Use

summaryto summarize the backtest results in a table format.

For more detailed information on this workflow, see Backtest Workflow and Backtest Investment Strategies Using Financial Toolbox.

Creation

Description

backtester = backtestEngine(strategies)backtestEngine object. Use the

backtestEngine object to backtest the portfolio

trading strategies defined in the backtestStrategy objects.

backtester = backtestEngine(___,Name,Value)backtester =

backtestEngine(strategies,'RiskFreeRate',0.02,'InitialPortfolioValue',1000,'RatesConvention',"Annualized",'Basis',2).

Input Arguments

Name-Value Arguments

Output Arguments

Properties

Object Functions

runBacktest | Run backtest on one or more strategies |

summary | Generate summary table of backtest results |

equityCurve | Plot equity curves of strategies |

Examples

Use a backtesting engine in MATLAB® to run a backtest on an investment strategy over a time series of market data. You can define a backtesting engine by using backtestEngine object. A backtestEngine object sets properties of the backtesting environment, such as the risk-free rate, and holds the results of the backtest. In this example, you can create a backtesting engine to run a simple backtest and examine the results.

Create Strategy

Define an investment strategy by using the backtestStrategy function. This example builds a simple equal-weighted investment strategy that invests equally across all assets. For more information on creating backtest strategies, see backtestStrategy.

% The rebalance function is simple enough that you can use an anonymous function equalWeightRebalanceFcn = @(current_weights,~) ones(size(current_weights)) / numel(current_weights); % Create the strategy strategy = backtestStrategy("EqualWeighted",equalWeightRebalanceFcn,... 'RebalanceFrequency',20,... 'TransactionCosts',[0.0025 0.005],... 'LookbackWindow',0)

strategy =

backtestStrategy with properties:

Name: "EqualWeighted"

RebalanceFcn: @(current_weights,~)ones(size(current_weights))/numel(current_weights)

RebalanceFrequency: 20

TransactionCosts: [0.0025 0.0050]

LookbackWindow: 0

InitialWeights: [1×0 double]

ManagementFee: 0

ManagementFeeSchedule: 1y

PerformanceFee: 0

PerformanceFeeSchedule: 1y

PerformanceHurdle: 0

UserData: [0×0 struct]

EngineDataList: [0×0 string]

Set Backtesting Engine Properties

The backtesting engine has several properties that you set by using parameters to the backtestEngine function.

Risk-Free Rate

The RiskFreeRate property holds the interest rate earned for uninvested capital (that is, cash). When the sum of portfolio weights is below 1, the remaining capital is invested in cash and earns the risk-free rate. The risk-free rate and the cash-borrow rate can be defined in annualized terms or as explicit "per-time-step" interest rates. The RatesConvention property is used to specify how the backtestEngine interprets the two rates (the default interpretation is "Annualized"). For this example, set the risk-free rate to 2% annualized.

% 2% annualized risk-free rate

riskFreeRate = 0.02;Cash Borrow Rate

The CashBorrowRate property sets the interest accrual rate applied to negative cash balances. If at any time the portfolio weights sum to a value greater than 1, then the cash position is negative by the amount in excess of 1. This behavior of portfolio weights is analogous to borrowing capital on margin to invest with leverage. Like the RiskFreeRate property, the CashBorrowRate property can either be annualized or per-time-step depending on the value of the RatesConvention property.

% 6% annualized margin interest rate

cashBorrowRate = 0.06;Initial Portfolio Value

The InitialPortfolioValue property sets the value of the portfolio at the start of the backtest for all strategies. The default is $10,000.

% Start backtest with $1M

initPortfolioValue = 1000000;Create Backtest Engine

Using the prepared properties, create the backtesting engine using the backtestEngine function.

% The backtesting engine takes an array of backtestStrategy objects as the first argument backtester = backtestEngine(strategy,... 'RiskFreeRate',riskFreeRate,... 'CashBorrowRate',cashBorrowRate,... 'InitialPortfolioValue',initPortfolioValue)

backtester =

backtestEngine with properties:

Strategies: [1×1 backtestStrategy]

RiskFreeRate: 0.0200

CashBorrowRate: 0.0600

RatesConvention: "Annualized"

Basis: 0

InitialPortfolioValue: 1000000

DateAdjustment: "Previous"

PayExpensesFromCash: 0

NumAssets: []

Returns: []

Positions: []

Turnover: []

BuyCost: []

SellCost: []

TransactionCosts: []

Fees: []

Several additional properties of the backtesting engine are initialized to empty. The backtesting engine populates these properties, which contain the results of the backtest, upon completion of the backtest.

Load Data and Run Backtest

Run the backtest over daily price data from the 30 component stocks of the DJIA.

% Read table of daily adjusted close prices for 2006 DJIA stocks T = readtable('dowPortfolio.xlsx'); % Remove the DJI index column and convert to timetable pricesTT = table2timetable(T(:,[1 3:end]),'RowTimes','Dates');

Run the backtest using the runBacktest function.

backtester = runBacktest(backtester,pricesTT)

backtester =

backtestEngine with properties:

Strategies: [1×1 backtestStrategy]

RiskFreeRate: 0.0200

CashBorrowRate: 0.0600

RatesConvention: "Annualized"

Basis: 0

InitialPortfolioValue: 1000000

DateAdjustment: "Previous"

PayExpensesFromCash: 0

NumAssets: 30

Returns: [250×1 timetable]

Positions: [1×1 struct]

Turnover: [250×1 timetable]

BuyCost: [250×1 timetable]

SellCost: [250×1 timetable]

TransactionCosts: [1×1 struct]

Fees: [1×1 struct]

Examine Results

The backtesting engine populates the read-only properties of the backtestEngine object with the backtest results. Daily values for portfolio returns, asset positions, turnover, transaction costs, and fees are available to examine.

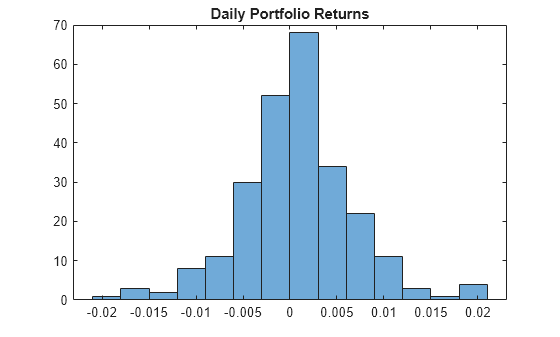

Examine the daily returns.

% Generate a histogram of daily portfolio returns histogram(backtester.Returns{:,1}) title('Daily Portfolio Returns')

Use equityCurve to plot the equity curve for the simple equal-weighted investment strategy.

equityCurve(backtester)

More About

Backtesting a portfolio of investments refers to the process of applying a trading strategy to historical or simulated market data to determine how accurately the strategy would have predicted actual results.

The steps of the backtesting workflow are:

Strategy definition — Clearly define the investment strategy, including the selection criteria for assets, the timing of buy and sell decisions, portfolio rebalancing rules, risk management techniques, and any other relevant parameters using

backtestStrategy.Create backtest engine — Use

backtestEngineto create the framework designed to facilitate the backtesting of investment strategies using historical data.Define historical or simulated market data — Collect historical market data that is relevant to the strategy. This could include price data, trading volumes, economic indicators, or any other data that the strategy requires.

Run backtest — Use

runBacktestto apply the investment strategy to the historical data to simulate how the portfolio would have performed during the selected time period. This involves "pretend" buying and selling assets according to the rules of the strategy.Analyze results — Use

summaryandequityCurvecalculate performance metrics from the simulated historical performance. Typical metrics include total return, annualized return, risk measures like standard deviation or maximum drawdown, and risk-adjusted return measures like the Sharpe ratio. Analyze the results to determine the potential effectiveness of the strategy. This includes looking for periods of underperformance, assessing the strategy's consistency, and comparing it to benchmarks or alternative strategies.Refine strategies — Based on the analysis, refine the strategy to improve its performance or to reduce risk. This step may involve adjusting the rules, incorporating additional data, or altering the portfolio composition. To avoid overfitting, the strategy should be validated using out-of-sample data—data that was not used in the initial backtesting. This helps ensure that the strategy is robust and not just tailored to the specific historical period initially tested.

Version History

Introduced in R2020bSee Also

backtestStrategy | runBacktest | summary | equityCurve | timetable

Topics

- Backtest Investment Strategies Using Financial Toolbox

- Backtest Investment Strategies with Trading Signals

- Backtest Investment Strategies Using datetime and calendarDuration

- Backtest Using Risk-Based Equity Indexation

- Backtest with Brinson Attribution to Evaluate Portfolio Performance

- runBacktest Processing Steps