runBacktest

Run backtest on one or more strategies

Syntax

Description

backtester = runBacktest(backtester,pricesTT)

runBacktest initializes each strategy previously defined using

backtestStrategy to the

InitialPortfolioValue and then begins processing the timetable of

price data (pricesTT) as follows:

At each time step, the

runBacktestfunction applies the asset returns to the strategy portfolio positions.The

runBacktestfunction determines which strategies to rebalance based on theRebalanceFrequencyproperty of thebacktestStrategyobjects.For strategies that need rebalancing, the

runBacktestfunction calls their rebalance functions with a rolling window of asset price data based on theLookbackWindowproperty of eachbacktestStrategy.Transaction costs are calculated and charged based on the changes in asset positions and the

TransactionCostsproperty of eachbacktestStrategyobject.After the backtest is complete, the results are stored in several properties of the

backtestEngineobject. For more information, see runBacktest Processing Steps.

backtester = runBacktest(backtester,pricesTT,signalTT)signalTT), then the

runBacktest function runs the backtest and additionally passes a

rolling window of signal data to the rebalance function of each strategy during the

rebalance step.

backtester

= runBacktest(___,Name,Value)backtester =

runBacktest(backtester,assetPrices,'Start',50,'End',100).

Examples

The MATLAB® backtesting engine runs backtests of portfolio investment strategies over timeseries of asset price data. After creating a set of backtest strategies using backtestStrategy and the backtest engine using backtestEngine, the runBacktest function executes the backtest. This example illustrates how to use the runBacktest function to test investment strategies.

Load Data

Load one year of stock price data. For readability, this example only uses a subset of the DJIA stocks.

% Read table of daily adjusted close prices for 2006 DJIA stocks T = readtable('dowPortfolio.xlsx'); % Prune the table on only hold the dates and selected stocks timeColumn = "Dates"; assetSymbols = ["BA", "CAT", "DIS", "GE", "IBM", "MCD", "MSFT"]; T = T(:,[timeColumn assetSymbols]); % Convert to timetable pricesTT = table2timetable(T,'RowTimes','Dates'); % View the final asset price timetable head(pricesTT)

Dates BA CAT DIS GE IBM MCD MSFT

___________ _____ _____ _____ _____ _____ _____ _____

03-Jan-2006 68.63 55.86 24.18 33.6 80.13 32.72 26.19

04-Jan-2006 69.34 57.29 23.77 33.56 80.03 33.01 26.32

05-Jan-2006 68.53 57.29 24.19 33.47 80.56 33.05 26.34

06-Jan-2006 67.57 58.43 24.52 33.7 82.96 33.25 26.26

09-Jan-2006 67.01 59.49 24.78 33.61 81.76 33.88 26.21

10-Jan-2006 67.33 59.25 25.09 33.43 82.1 33.91 26.35

11-Jan-2006 68.3 59.28 25.33 33.66 82.19 34.5 26.63

12-Jan-2006 67.9 60.13 25.41 33.25 81.61 33.96 26.48

Create Strategy

In this introductory example, test an equal weighted investment strategy. This strategy invests an equal portion of the available capital into each asset. This example does describe the details about how to create backtest strategies. For more information on creating backtest strategies, see backtestStrategy.

Set the RebalanceFrequency to rebalance the portfolio every 60 days. This example does not use a lookback window to rebalance.

% Create the strategy numAssets = size(pricesTT,2); equalWeightsVector = ones(1,numAssets) / numAssets; equalWeightsRebalanceFcn = @(~,~) equalWeightsVector; ewStrategy = backtestStrategy("EqualWeighted",equalWeightsRebalanceFcn, ... 'RebalanceFrequency',60, ... 'LookbackWindow',0, ... 'TransactionCosts',0.005, ... 'InitialWeights',equalWeightsVector)

ewStrategy =

backtestStrategy with properties:

Name: "EqualWeighted"

RebalanceFcn: @(~,~)equalWeightsVector

RebalanceFrequency: 60

TransactionCosts: 0.0050

LookbackWindow: 0

InitialWeights: [0.1429 0.1429 0.1429 0.1429 0.1429 0.1429 0.1429]

ManagementFee: 0

ManagementFeeSchedule: 1y

PerformanceFee: 0

PerformanceFeeSchedule: 1y

PerformanceHurdle: 0

UserData: [0×0 struct]

EngineDataList: [0×0 string]

Run Backtest

Create a backtesting engine and run a backtest over a year of stock data. For more information on creating backtest engines, see backtestEngine.

% Create the backtest engine. The backtest engine properties that hold the % results are initialized to empty. backtester = backtestEngine(ewStrategy)

backtester =

backtestEngine with properties:

Strategies: [1×1 backtestStrategy]

RiskFreeRate: 0

CashBorrowRate: 0

RatesConvention: "Annualized"

Basis: 0

InitialPortfolioValue: 10000

DateAdjustment: "Previous"

PayExpensesFromCash: 0

NumAssets: []

Returns: []

Positions: []

Turnover: []

BuyCost: []

SellCost: []

TransactionCosts: []

Fees: []

% Run the backtest. The empty properties are now populated with % timetables of detailed backtest results. backtester = runBacktest(backtester,pricesTT)

backtester =

backtestEngine with properties:

Strategies: [1×1 backtestStrategy]

RiskFreeRate: 0

CashBorrowRate: 0

RatesConvention: "Annualized"

Basis: 0

InitialPortfolioValue: 10000

DateAdjustment: "Previous"

PayExpensesFromCash: 0

NumAssets: 7

Returns: [250×1 timetable]

Positions: [1×1 struct]

Turnover: [250×1 timetable]

BuyCost: [250×1 timetable]

SellCost: [250×1 timetable]

TransactionCosts: [1×1 struct]

Fees: [1×1 struct]

Backtest Summary

Use the summary function to generate a summary table of backtest results.

% Examing results. The summary table shows several performance metrics.

summary(backtester)ans=9×1 table

EqualWeighted

_____________

TotalReturn 0.22943

SharpeRatio 0.11415

Volatility 0.0075013

AverageTurnover 0.00054232

MaxTurnover 0.038694

AverageReturn 0.00085456

MaxDrawdown 0.098905

AverageBuyCost 0.030193

AverageSellCost 0.030193

When running a backtest in MATLAB®, you need to understand what the initial conditions are when the backtest begins. The initial weights for each strategy, the size of the strategy lookback window, and any potential split of the dataset into training and testing partitions affects the results of the backtest. This example shows how to use the runBacktest function with the 'Start' and 'End' name-value pair arguments that interact with the LookbackWindow and RebalanceFrequency properties of the backtestStrategy object to "warm start" a backtest.

Load Data

Load one year of stock price data. For readability, this example uses only a subset of the DJIA stocks.

% Read table of daily adjusted close prices for 2006 DJIA stocks. T = readtable('dowPortfolio.xlsx'); % Prune the table to include only the dates and selected stocks. timeColumn = "Dates"; assetSymbols = ["BA", "CAT", "DIS", "GE", "IBM", "MCD", "MSFT"]; T = T(:,[timeColumn assetSymbols]); % Convert to timetable. pricesTT = table2timetable(T,'RowTimes','Dates'); % View the final asset price timetable. head(pricesTT)

Dates BA CAT DIS GE IBM MCD MSFT

___________ _____ _____ _____ _____ _____ _____ _____

03-Jan-2006 68.63 55.86 24.18 33.6 80.13 32.72 26.19

04-Jan-2006 69.34 57.29 23.77 33.56 80.03 33.01 26.32

05-Jan-2006 68.53 57.29 24.19 33.47 80.56 33.05 26.34

06-Jan-2006 67.57 58.43 24.52 33.7 82.96 33.25 26.26

09-Jan-2006 67.01 59.49 24.78 33.61 81.76 33.88 26.21

10-Jan-2006 67.33 59.25 25.09 33.43 82.1 33.91 26.35

11-Jan-2006 68.3 59.28 25.33 33.66 82.19 34.5 26.63

12-Jan-2006 67.9 60.13 25.41 33.25 81.61 33.96 26.48

Create Strategy

This example backtests an "inverse variance" strategy. The inverse variance rebalance function is implemeted in the Local Functions section. For more information on creating backtest strategies, see backtestStrategy. The inverse variance strategy uses the covariance of asset returns to make decisions about asset allocation. The LookbackWindow for this strategy must contain at least 30 days of trailing data (about 6 weeks), and at most, 60 days (about 12 weeks).

Set RebalanceFrequency for backtestStrategy to rebalance the portfolio every 25 days.

% Create the strategy minLookback = 30; maxLookback = 60; ivStrategy = backtestStrategy("InverseVariance",@inverseVarianceFcn, ... 'RebalanceFrequency',25, ... 'LookbackWindow',[minLookback maxLookback], ... 'TransactionCosts',[0.0025 0.005])

ivStrategy =

backtestStrategy with properties:

Name: "InverseVariance"

RebalanceFcn: @inverseVarianceFcn

RebalanceFrequency: 25

TransactionCosts: [0.0025 0.0050]

LookbackWindow: [30 60]

InitialWeights: [1×0 double]

ManagementFee: 0

ManagementFeeSchedule: 1y

PerformanceFee: 0

PerformanceFeeSchedule: 1y

PerformanceHurdle: 0

UserData: [0×0 struct]

EngineDataList: [0×0 string]

Run Backtest and Examine Results

Create a backtesting engine and run a backtest over a year of stock data. For more information on creating backtest engines, see backtestEngine.

% Create the backtest engine. backtester = backtestEngine(ivStrategy); % Run the backtest. backtester = runBacktest(backtester,pricesTT);

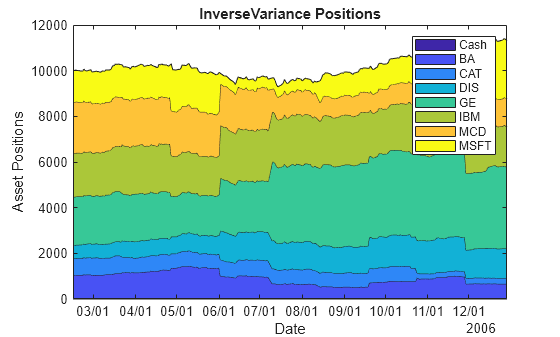

Use the assetAreaPlot helper function, defined in the Local Functions section of this example, to display the change in the asset allocation over the course of the backtest.

assetAreaPlot(backtester,"InverseVariance")

Notice that the inverse variance strategy begins all in cash and remains in that state for about 2.5 months. This is because the backtestStrategy object does not have a specified set of initial weights, which you specify using the InitialPortfolioValue name-value pair argument. The inverse variance strategy requires 30 days of trailing asset price history before rebalancing. You can use the printRebalanceTable helper function, defined in the Local Functions section, to display the rebalance schedule.

printRebalanceTable(ivStrategy,pricesTT,minLookback);

First Day of Data Backtest Start Date Minimum Days to Rebalance

_________________ ___________________ _________________________

03-Jan-2006 03-Jan-2006 30

Rebalance Dates Days of Available Price History Enough Data to Rebalance

_______________ _______________________________ ________________________

08-Feb-2006 26 "No"

16-Mar-2006 51 "Yes"

21-Apr-2006 76 "Yes"

26-May-2006 101 "Yes"

03-Jul-2006 126 "Yes"

08-Aug-2006 151 "Yes"

13-Sep-2006 176 "Yes"

18-Oct-2006 201 "Yes"

22-Nov-2006 226 "Yes"

29-Dec-2006 251 "Yes"

The first rebalance date comes on February 8 but the strategy does not have enough price history to fill out a valid lookback window (minimum is 30 days), so no rebalance occurs. The next rebalance date is on March 16, a full 50 days into the backtest.

This situation is not ideal as these 50 days sitting in an all-cash position represent approximately 20% of the total backtest. Consequently, when the backtesting engine reports on the performance of the strategy (that is, the total return, Sharpe ratio, volatility, and so on), the results do not reflect the "true" strategy performance because the strategy only began to make asset allocation decisions only about 20% into the backtest.

Warm Start Backtest

It is possible to "warm start" the backtest. A warm start means that the backtest results reflect the strategy performance in the market conditions reflected in the price timetable. To start, set the initial weights of the strategy to avoid starting all in cash.

The inverse variance strategy requires 30 days of price history to fill out a valid lookback window, so you can partition the price data set into two sections, a "warm-up" set and a "test" set.

warmupRange = 1:30; % The 30th row is included in both ranges since the day 30 price is used % to compute the day 31 returns. testRange = 30:height(pricesTT);

Use the warm-up partition to set the initial weights of the inverse variance strategy. By doing so, you can begin the backtest with the strategy already "running" and avoid the initial weeks spent in the cash position.

% Use the rebalance function to set the initial weights. This might % or might not be possible for other strategies depending on the details of % the strategy logic. initWeights = inverseVarianceFcn([],pricesTT(warmupRange,:));

Update the strategy and rerun the backtest. Since the warm-up range is used to initialize the inverse variance strategy, you must omit this data from the backtest to avoid a look-ahead bias, or "seeing the future," and to backtest only over the "test range."

% Set the initial weights on the strategy in the backtester. You can do this when you % create the strategy as well, using the 'InitialWeights' parameter. backtester.Strategies(1).InitialWeights = initWeights; % Rerun the backtest over the "test" range. backtester = runBacktest(backtester,pricesTT(testRange,:));

When you generate the area plot, you can see that the issue where the strategy is in cash for the first portion of the backtest is avoided.

assetAreaPlot(backtester,"InverseVariance")

However, if you look at the rebalance table, you can see that the strategy still "missed" the first rebalance date. When you run the backtest over the test range of the data set, the first rebalance date is on March 22. This is because the warm-up range is omitted from the price history and the strategy had only 26 days of history available on that date (less than the minimum 30 days required for the lookback window). Therefore, the March 22 rebalance is skipped.

To avoid backtesting over the warm-up range, the range was removed it from the data set. This means the new backtest start date and all subsequent rebalance dates are 30 days later. The price history data contained in the warm-up range was completely removed, so when the backtest engine hit the first rebalance date the price history was insufficient to rebalance.

printRebalanceTable(ivStrategy,pricesTT(testRange,:),minLookback);

First Day of Data Backtest Start Date Minimum Days to Rebalance

_________________ ___________________ _________________________

14-Feb-2006 14-Feb-2006 30

Rebalance Dates Days of Available Price History Enough Data to Rebalance

_______________ _______________________________ ________________________

22-Mar-2006 26 "No"

27-Apr-2006 51 "Yes"

02-Jun-2006 76 "Yes"

10-Jul-2006 101 "Yes"

14-Aug-2006 126 "Yes"

19-Sep-2006 151 "Yes"

24-Oct-2006 176 "Yes"

29-Nov-2006 201 "Yes"

This scenario is also not correct since the original price timetable (warm-up and test partitions together) does have enough price history by March 22 to fill out a valid lookback window. However, the earlier data is not available to the backtest engine because the backtest was run using only the test partition.

Use Start and End Parameters for runBacktest

The ideal workflow in this situation is to both omit the warm-up data range from the backtest to avoid the look-ahead bias but include the warm-up data in the price history to be able to fill out the lookback window of the strategy with all available price history data. You can do so by using the 'Start' parameter for the runBacktest function.

The 'Start' and 'End' name-value pair arguments for runBacktest enable you to start and end the backtest on specific dates. You can specify 'Start' and 'End' as rows of the prices timetable or as datetime values (see the documentation for the runBacktest function for details). The 'Start' argument lets the backtest begin on a particular date while giving the backtest engine access to the full data set.

Rerun the backtest using the 'Start' name-value pair argument rather than only running on a partition of the original data set.

% Rerun the backtest starting on the last day of the warmup range. startRow = warmupRange(end); backtester = runBacktest(backtester,pricesTT,'Start',startRow);

Plot the new asset area plot.

assetAreaPlot(backtester,"InverseVariance")

View the new rebalance table with the new 'Start' parameter.

printRebalanceTable(ivStrategy,pricesTT,minLookback,startRow);

First Day of Data Backtest Start Date Minimum Days to Rebalance

_________________ ___________________ _________________________

03-Jan-2006 14-Feb-2006 30

Rebalance Dates Days of Available Price History Enough Data to Rebalance

_______________ _______________________________ ________________________

22-Mar-2006 55 "Yes"

27-Apr-2006 80 "Yes"

02-Jun-2006 105 "Yes"

10-Jul-2006 130 "Yes"

14-Aug-2006 155 "Yes"

19-Sep-2006 180 "Yes"

24-Oct-2006 205 "Yes"

29-Nov-2006 230 "Yes"

The inverse variance strategy now has enough data to rebalance on the first rebalance date (March 22) and the backtest is "warm started." By using the original data set, the first day of data remains January 3, and the 'Start' parameter allows you to move the backtest start date forward to avoid the warm-up range.

Even though the results are not dramatically different, this example illustrates the interaction between the LookbackWindow and RebalanceFrequency name-value arguments for a backtestStrategy object and the range of data used in the runBacktest when you evaluate the performance of a strategy in a backtest.

Local Functions

The strategy rebalance function is implemented as follows. For more information on creating strategies and writing rebalance functions, see backtestStrategy.

function new_weights = inverseVarianceFcn(current_weights, pricesTT) % Inverse-variance portfolio allocation. assetReturns = tick2ret(pricesTT); assetCov = cov(assetReturns{:,:}); new_weights = 1 ./ diag(assetCov); new_weights = new_weights / sum(new_weights); end

This helper function plots the asset allocation as an area plot.

function assetAreaPlot(backtester,strategyName) t = backtester.Positions.(strategyName).Time; positions = backtester.Positions.(strategyName).Variables; h = area(t,positions); title(sprintf('%s Positions',strategyName)); xlabel('Date'); ylabel('Asset Positions'); xtickformat('MM/dd'); xlim([t(1) t(end)]) oldylim = ylim; ylim([0 oldylim(2)]); cm = parula(numel(h)); for i = 1:numel(h) set(h(i),'FaceColor',cm(i,:)); end legend(backtester.Positions.(strategyName).Properties.VariableNames) end

This helper function generates a table of rebalance dates along with the available price history at each date.

function printRebalanceTable(strategy,pricesTT,minLookback,startRow) if nargin < 4 startRow = 1; end allDates = pricesTT.(pricesTT.Properties.DimensionNames{1}); rebalanceDates = allDates(startRow:strategy.RebalanceFrequency:end); [~,rebalanceIndices] = ismember(rebalanceDates,pricesTT.Dates); disp(table(allDates(1),rebalanceDates(1),minLookback,'VariableNames',{'First Day of Data','Backtest Start Date','Minimum Days to Rebalance'})); fprintf('\n\n'); numHistory = rebalanceIndices(2:end); sufficient = repmat("No",size(numHistory)); sufficient(numHistory > minLookback) = "Yes"; disp(table(rebalanceDates(2:end),rebalanceIndices(2:end),sufficient,'VariableNames',{'Rebalance Dates','Days of Available Price History','Enough Data to Rebalance'})); end