icdf

Inverse cumulative distribution function

Syntax

Description

Examples

Compute the icdf values for a normal distribution by specifying the distribution name 'Normal' and the distribution parameters.

Define the input vector p to contain the probability values at which to calculate the icdf.

p = [0.1,0.25,0.5,0.75,0.9];

Compute the icdf values for the normal distribution with the mean equal to 1 and the standard deviation equal to 5.

mu = 1;

sigma = 5;

y = icdf('Normal',p,mu,sigma)y = 1×5

-5.4078 -2.3724 1.0000 4.3724 7.4078

Each value in y corresponds to a value in the input vector x. For example, at the value x equal to 1, the corresponding icdf value y is equal to 7.4078.

Create a normal distribution object and compute the icdf values of the normal distribution using the object.

Create a normal distribution object with the mean equal to 1 and the standard deviation equal to 5.

mu = 1; sigma = 5; pd = makedist('Normal','mu',mu,'sigma',sigma);

Define the input vector p to contain the probability values at which to calculate the icdf.

p = [0.1,0.25,0.5,0.75,0.9];

Compute the icdf values for the normal distribution at the values in p.

x = icdf(pd,p)

x = 1×5

-5.4078 -2.3724 1.0000 4.3724 7.4078

Each value in x corresponds to a value in the input vector p. For example, at the value p equal to 0.9, the corresponding icdf value x is equal to 7.4078.

Create a Poisson distribution object with the rate parameter, , equal to 2.

lambda = 2; pd = makedist('Poisson','lambda',lambda);

Define the input vector p to contain the probability values at which to calculate the icdf.

p = [0.1,0.25,0.5,0.75,0.9];

Compute the icdf values for the Poisson distribution at the values in p.

x = icdf(pd,p)

x = 1×5

0 1 2 3 4

Each value in x corresponds to a value in the input vector p. For example, at the value p equal to 0.9, the corresponding icdf value x is equal to 4.

Alternatively, you can compute the same icdf values without creating a probability distribution object. Use the icdf function and specify a Poisson distribution using the same value for the rate parameter .

x2 = icdf('Poisson',p,lambda)x2 = 1×5

0 1 2 3 4

The icdf values are the same as those computed using the probability distribution object.

Create a standard normal distribution object.

pd = makedist('Normal')pd =

NormalDistribution

Normal distribution

mu = 0

sigma = 1

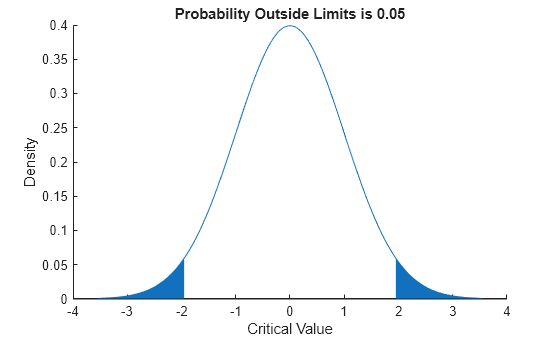

Determine the critical values at the 5% significance level for a test statistic with a standard normal distribution, by computing the upper and lower 2.5% values.

x = icdf(pd,[.025,.975])

x = 1×2

-1.9600 1.9600

Plot the cdf and shade the critical regions.

p = normspec(x,0,1,'outside')

p = 0.0500

Input Arguments

Output Arguments

Alternative Functionality

icdf is a generic function that accepts either a distribution by

its name name or a probability distribution object

pd. It is faster to use a distribution-specific function, such

as norminv for the normal distribution and

binoinv for the binomial distribution.

For a list of distribution-specific functions, see Supported Distributions.

Extended Capabilities

Version History

Introduced before R2006a

See Also

cdf | mle | pdf | random | makedist | fitdist | Distribution Fitter | paretotails